Highlights

- China's dominance in rare earth magnet production (90%+) creates a critical chokepoint for EV manufacturing, with availability now selectively allocated rather than freely accessible to Western automakers.

- Non-rare-earth solutions like iron-nitride magnets and magnet-free motor architectures are advancing but face qualification, cost, and manufacturing challenges that push realistic scale to 2030-2033.

- If Chinese magnet supply is disrupted, the auto industry will respond with tactical triage—prioritizing high-margin vehicles, rapidly redesigning auxiliary systems, and accelerating recycling rather than wholesale replacement.

The automotive sector’s vulnerability is not merely about rare earth scarcity—it is about control. The chokepoint lies in the conversion of oxides into qualified magnets, where China maintains overwhelming dominance. And let’s not forget, those magnets are customized to specific product inputs. Estimates consistently place China at roughly 85% of global refining capacity and over 90% of rare earth magnet production, creating a systemic single point of failure across the EV supply chain. Recent trade data reinforces a critical shift in how risk manifests. In early 2026, China’s rare earth magnet exports increased overall, yet shipments to the United States declined sharply. The implication is clear: availability is not the same as access. Supply exists—but it is selectively allocated via China.

At the same time, licensing delays and export controls are now operational risks. Magnets are embedded across dozens of vehicle subsystems—from traction motors to braking and ADAS—meaning disruption at the magnet level cascades quickly into production slowdowns or shutdowns. Compounding this risk, heavy rare earth supply (dysprosium, terbium) remains partially dependent on unstable upstream flows from Myanmar, adding a geopolitical fragility layer that is often underestimated.

Yes, a handful of prominent mine-to-magnet and cyclical/recycling projects are funded by the American government. And Rare Earth Exchanges™ forecasts that, by at least 2029 to 2030, some of those investments will achieve the scale touted today.

So how is the automobile OEM supply chain responding to this crisis?

The Non-Rare-Earth Toolkit: Magnets vs. Motors

At a high level, the industry response has bifurcated into two distinct innovation pathways:

1. Alternative Magnet Materials (Non-NdFeB)

Companies like Niron Magnetics (opens in a new tab) are advancing iron-nitride permanent magnets—promising comparable performance without rare earth inputs. The company has raised significant capital and is targeting large-scale production toward the late decade (2028–2029). Will they achieve this general milestone? Rare Earth Exchanges continues to monitor as part of our broader supply chain rankings and risk signal detection.

Importantly, the gating factors facing Niron remain formidable:

- Industrial yield and consistency

- Cost competitiveness vs. Chinese NdFeB

- Multi-year automotive qualification cycles

For the reasons above and others, the risk of timeline delay is substantial.

2. Magnet-Free Motor Architectures

Suppliers such as ZF Friedrichshafen and BorgWarner are advancing electrically excited and inductive motor designs that eliminate permanent magnets entirely.

Examples include:

- ZF’s I²SM architecture (opens in a new tab) (inductive rotor excitation)

- BorgWarner + Oak Ridge National Laboratory wireless excitation systems (opens in a new tab)

These technologies are no longer theoretical—they demonstrate strong performance metrics—but remain pre-scale in automotive production terms.

Meanwhile, OEM timelines reinforce the lag:

- Renault targets rare-earth-free motors around 2028

- Astemo points to ~2030 for practical deployment

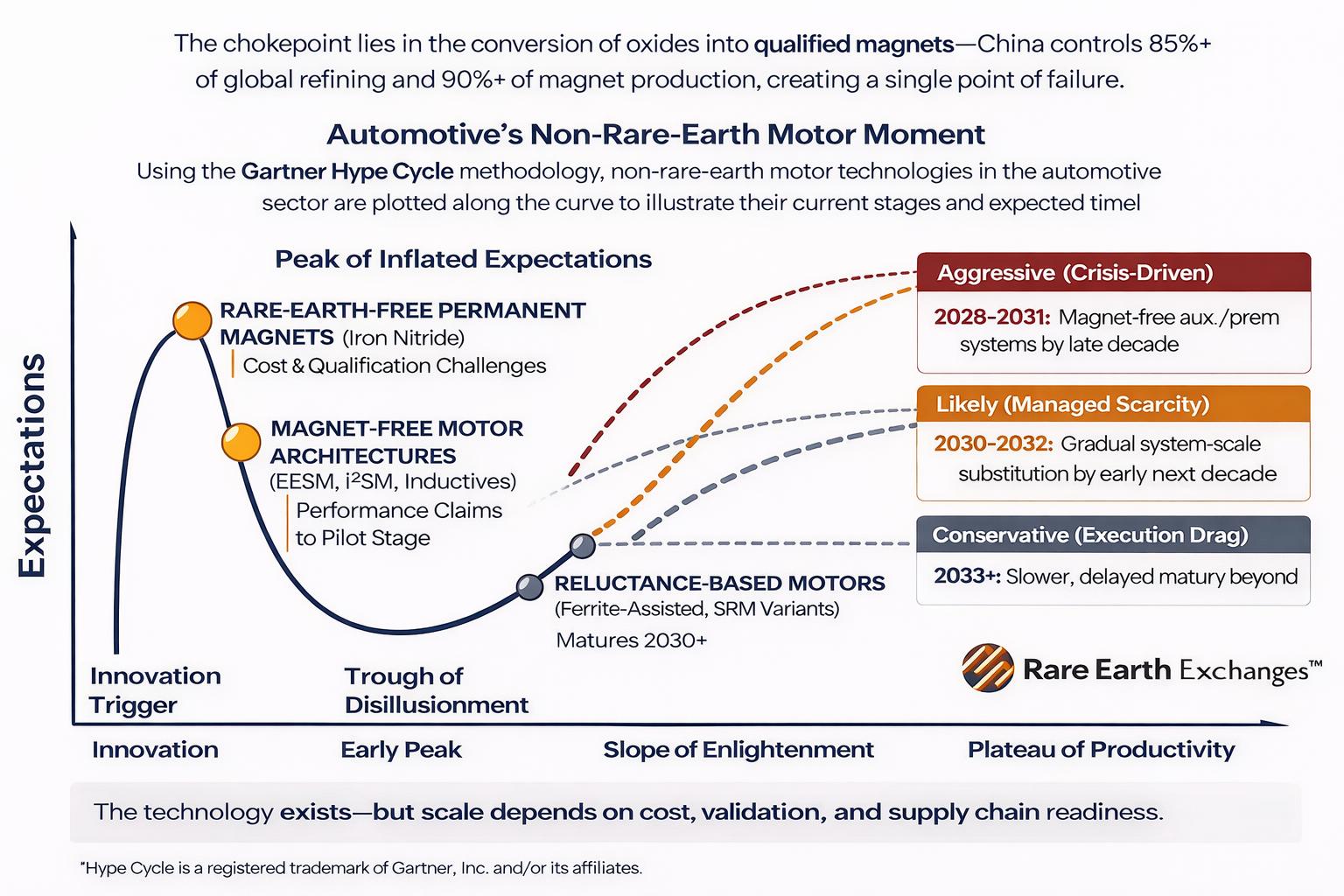

Where We Are on the ‘Hype Cycle’

Using the Gartner Hype Cycle (opens in a new tab) research methodology as a framework, non-rare-earth technologies are progressing—but unevenly. Below Rare Earth Exchanges provides an update:

| Technology | Stage in Cycle | Summary |

|---|---|---|

| Rare-Earth-Free Permanent Magnets (Iron Nitride) | Peak of Inflated Expectations | Capital inflows and factory announcements are accelerating. But industrialization risk remains high. The next phase will likely expose cost, yield, and qualification challenges |

| Magnet-Free Motor Architectures (EESM, I²SM, Wireless Excitation) | Late Innovation Trigger → Early Peak | Performance claims are credible, and prototypes exist. But visibility into high-volume production commitments remains limited—a classic setup for expectation overshoot |

| Reluctance-Based Motors (Ferrite-assisted, SRM variants)Position | Early Slope of Enlightenment | Engineering tradeoffs are now understood (NVH, efficiency, packaging), but timelines still point to 2030+ for meaningful scale |

When Does Scale Actually Arrive? Three Scenarios

Rare Earth Exchanges puts forth three scenarios for deployment at scale.

| Scenario | Timeline | Adoption Pathway | Key Trigger/Constraint |

|---|---|---|---|

| Aggressive (Crisis-Driven) | 2028-2031 | Magnet-free solutions penetrate auxiliary and premium systems by 2028–2029; broader traction motor adoption begins 2029–2031 | Sustained supply shock or export embargo forces rapid redesign and substitution |

| Likely (Managed Scarcity) | 2030-2032 | Gradual substitution with auxiliaries first, traction later; system-level adoption reaches scale across platforms | Ongoing supply pressure with partial access; steady engineering and qualification progress |

| Conservative (Execution Drag) | 2033+ | Slow adoption due to technical hurdles; limited early deployment with delayed system-wide scale | Qualification delays, cost barriers, NVH/packaging challenges, and manufacturing scale constraints |

Key takeaway:

The technology exists—but qualification, at scale, not invention, sets the clock.

If China Supply Breaks: The Next 36 Months

If Chinese rare-earth magnets become intermittently unavailable, the industry response will not be elegant—it will be urgent and tactical.

Expect the following:

| Response Strategy | Key Actions | Implication for Industry |

|---|---|---|

| 1. Allocation, Not Replacement | Prioritize magnets for high-margin vehicles and safety-critical systems | Limited supply is triaged, protecting profitability and compliance over volume production |

| 2. Rapid Redesign of “Replaceable” Systems | Shift auxiliary motors (HVAC, pumps, sensors) to ferrite or magnet-free designs; redesign ADAS components where feasible | Fastest path to reduce dependence, but limited to non-core or flexible subsystems |

| 3. Inventory + Workarounds | Stockpile where possible; build vehicles without constrained components and hold inventory | Short-term continuity strategy, but creates working capital strain and operational inefficiency |

| 4. Recycling Acceleration | Scale magnet scrap recovery and reprocessing | Recycling becomes a strategic supply source, not just an ESG initiative |

| 5. Supplier-Level Substitution (Not OEM-Level) | Tier 1 and Tier 2 suppliers redesign systems and substitute materials | OEMs remain indirectly exposed; true control sits deeper in the supply chain |

The Bottom Line: Not a Materials Problem—A System Problem

Non-rare-earth motor technology is real. It is advancing. It will scale.

But not yet. The automotive industry is not facing a shortage of rare earths.

It is facing a crisis in control, access, and qualification above all else.

Until the West can:

- Refine at scale

- Manufacture magnets at scale

- Qualify them across automotive systems

…it does not control its own production destiny.

REEx Insight

The market is transitioning from materials dependency → system redesign.

And the battleground is not merely mining and refining. It is engineering, systems change, qualification, investment, talent, and time.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →