Highlights

- Major copper discoveries are declining while prices surge.

- The bigger vulnerability lies in who controls the refining: China dominates over 50% of global copper refining capacity.

- Four of the five largest smelters are located in China.

- The U.S. and West face a critical supply chain gap.

- Even if they mine more copper domestically, lack of refining infrastructure keeps them dependent on foreign processing.

- This situation mirrors the bottleneck seen in rare earth elements.

- For critical minerals supply chains, mining alone doesn't guarantee independence.

- Downstream processing concentration creates geopolitical leverage.

- Midstream refining capacity is just as strategic as extraction.

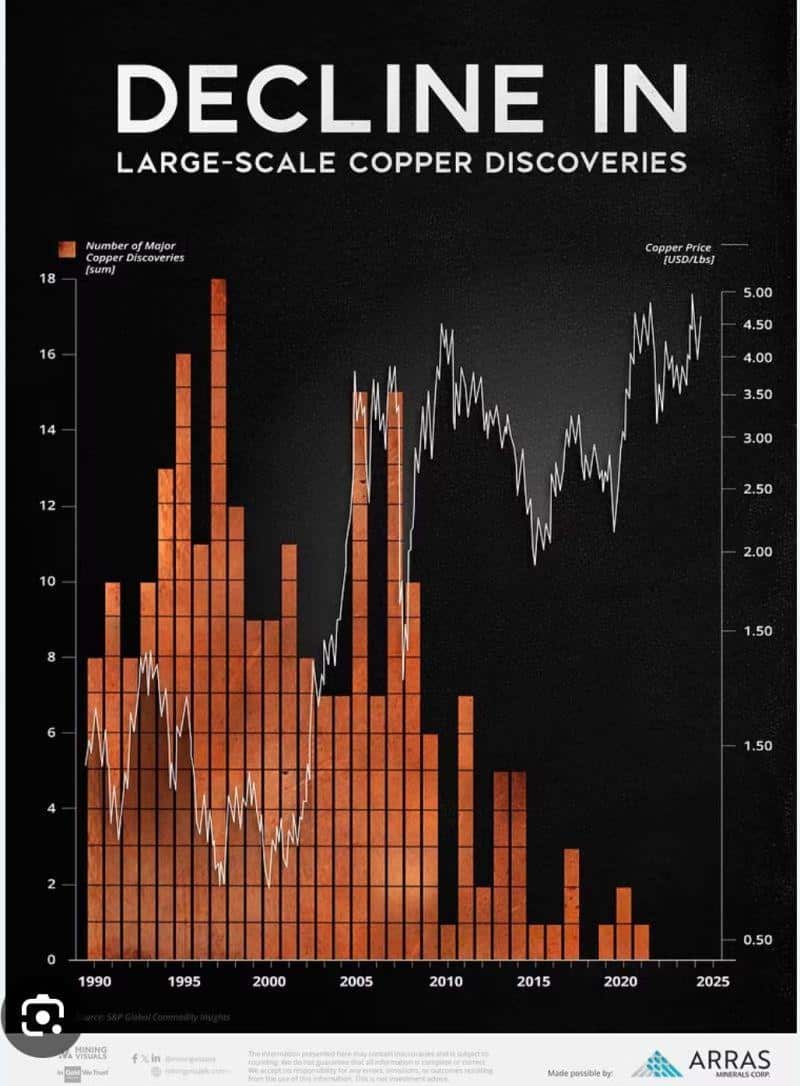

A recent chart shared online highlights a key structural problem: declining major copper discoveries even as prices surge. But there’s a companion dynamic that tends to get less play in the headlines — who dominates the refining and smelting stage of copper, and how that dominance affects supply chains.

Table of Contents

Copper Discoveries on the Wane

Who holds the furnace controls?

Midstream processing of copper (smelting + refining) is far less evenly distributed than mining. In fact:

- According to the International Copper Study Group (opens in a new tab) (ICSG), the top three refining countries already account for about 57% of global refined copper output.

- Recent commentary says that China alone probably accounts for over half of world refined copper production at present.

- For example, four of the largest five copper smelters are in mainland China.

Put simply, many countries may mine copper, but downstream processing, just like with rare earth elements, is heavily concentrated, and China sits at the center of that funnel.

Why this concentration?

Several reasons.

- Smelting and refining are capital-intensive and often scale with logistics, energy, and environmental control. China’s industrial policy has invested heavily in this midstream infrastructure.

- Many mines export concentrates rather than refined products, meaning the crude feedstock is available to large processing hubs. China imports ore, concentrates, or has outward investment into foreign mines and then does the refining.

- The processing side benefits from economies of scale, vertical integration, supply chain proximity (especially for downstream metals, wires, and consumer goods), and regulatory/industrial-policy support.

Why the U.S. & West should care

This concentration in refining is a vulnerability for Western supply chains, especially given the growing role of copper in electrification, renewable infrastructure, EVs, and defense. Key impacts:

- Even if the U.S. or Western countries mine more copper, if they lack the refining capacity, they remain dependent on foreign midstream infrastructure. For example, U.S. data show that while it produces significant copper, it still imports a large portion of refined copper. Reuters (opens in a new tab)

- If smelting/refining capacity is concentrated in one geography (China), geopolitical or supply disruptions (trade restrictions, environmental shutdowns, energy shocks) can ripple globally.

- For rare earth and other critical minerals sectors (which we track at Rare Earth Exchanges), this is a cautionary mirror: mining alone does not secure supply chain independence — the processing and refining downstream matter just as much.

- As copper discoveries decline and new large-scale finds become rarer, the bottleneck shifts upstream — but the mid-stream remains a choke-point. If you cannot add refining capacity easily, supply stress only intensifies.

What’s accurate, what’s speculative & what to watch

China’s dominance in refined copper production and smelting capacity is well established, and the combination of fewer large new discoveries and higher prices reflects a genuine structural constraint in global supply. The United States, meanwhile, remains heavily import-dependent due to its limited domestic refining base. However, claims read online that every tonne of mined copper must pass through China overstate the case—several nations, from Chile to Japan, refine substantial volumes locally or export finished cathodes.

Likewise, warnings of an imminent supply collapse are speculative; while concentration risk is real, the market can respond through new investment, recycling, and technological substitution. Forecast figures for future supply or discovery rates should also be treated cautiously, as directionally valid but imprecise in timing and scale.

Finally, much commentary risks overstating China’s role as a “villain” in the refining chain—its dominance stems as much from energy economics, logistics, and policy as from geopolitical intent—and narratives about a collapse in discoveries often overlook the ongoing though smaller-scale exploration successes still occurring worldwide.

Why this matters for rare earths & critical minerals

At Rare Earth Exchanges, we think in terms of complete supply chains. Although not a rare earth, but rather a critical mineral, copper reminds us: mining is only half the equation. For rare earths and critical minerals, if extraction occurs but refining or magnet production remains overseas, independence remains elusive. The mid-stream bottleneck in copper is essentially the same structural risk facing rare earths: downstream processing concentration = supply chain leverage. Again, the need for industrial policy becomes imminent.

©!-- /wp:paragraph -->

0 Comments