Highlights

- Saga Metals acquires the Wolverine REE Project in Labrador, featuring near-surface heavy rare earth mineralization with 24–28% HREO content including critical dysprosium and terbium.

- The deal structure involves significant equity dilution (4.25M shares + up to $5M in tranches) tied to aggressive milestones, with no NI 43-101 resource estimate or proven metallurgy yet.

- While the project offers geological optionality in a Tier-1 jurisdiction, it lacks critical commercialization elements: processing partnerships, offtake agreements, and validated separation pathways.

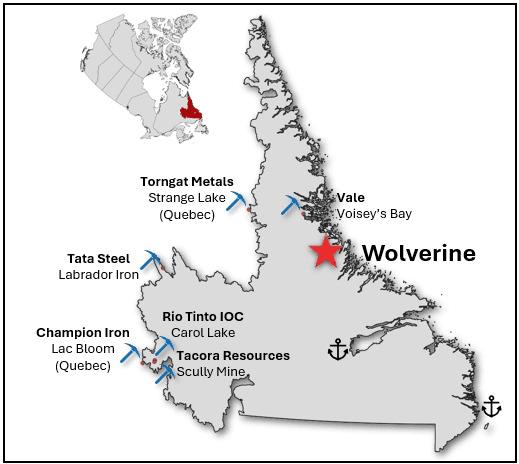

Saga Metals Corp. (TSXV: SAGA) announced (opens in a new tab) a definitive agreement to acquire the Wolverine REE Project, a 100%-owned, royalty-free asset in Labrador. The company highlights near-surface mineralization across a 1.7 km × 1.2 km footprint, with drill intercepts such as 48.8m at 0.77% TREO and peak grades exceeding 2% TREO. Notably, the project reports ~24–28% heavy rare earth oxide (HREO) content, including dysprosium and terbium—critical inputs for high-performance magnets in defense and EVs.

What Looks Attractive—On Paper

The Wolverine project checks several boxes investors look for:

- Heavy rare earth exposure (Dy, Tb)—the scarcest and most strategic segment

- Near-surface geometry—potentially lower strip ratios

- District-scale footprint (230+ km², largely underexplored)

- Located in a Tier-1 jurisdiction (Canada)

Management also draws comparisons to major deposits like Strange Lake and Tanbreez—though explicitly notes these are not verified equivalents.

Where Investors Should Be Skeptical

This is a promotional exploration-stage announcement. Key risks and gaps:

- No resource estimate yet (NI 43-101 pending)

- Metallurgy is unproven—critical for REE projects

- “Similar to Strange Lake” comparisons are speculative

- Only ~10% of the system was drilled

Most importantly:

➡ No processing pathway exists

Heavy rare earth projects are not won at the mine—they are won in separation and refining, where China still dominates ~90% of capacity.

Deal Structure Raises Questions

Saga is paying:

- 4.25M shares + $1M upfront

- Up to $5M share tranches + $1M cash per milestone

- Milestones tied to aggressive targets (e.g., $2.5B NPV, 30% IRR)

This structure is highly equity-dilutive and forward-loaded on optimistic assumptions.

Stock Perspective (Early-Stage Reality)

Saga Metals remains a micro-cap exploration story:

- No revenue

- Multi-asset diversification (uranium, lithium, titanium, REEs)

- High dilution risk is typical of junior miners

Technically, such stocks trade on narrative cycles—REE news can drive spikes, but sustainability depends on resource definition and financing.

REEx Critical Take

The announcement is technically credible but strategically incomplete.

Yes—heavy rare earth exposure in Canada is valuable.

But without:

- Processing partnerships

- Offtake agreements

- Metallurgical validation

…this remains geological optionality, not supply chain reality.

The Bigger Question for Investors

- What are timelines in the development process?

- Who will process Wolverine’s HREOs?

- How will Saga compete against Chinese cost structures?

- Can this asset attract DoD or strategic capital?

- Is this a discovery story—or a dilution story?

REEx Bottom Line

Saga’s Wolverine acquisition is a high-upside, high-risk exploration play aligned with Western supply chain ambitions—but far from execution.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →