Highlights

- A 2026 University of Texas study reveals that while battery metals like lithium, cobalt, and nickel are mined globally, real control is concentrated in a few companies and processing hubs, especially in East Asia, creating hidden supply chain vulnerabilities.

- Processing and refining, not mining, is the real bottleneck: cobalt refining is dominated by China, manganese by a few firms, while copper and aluminum depend heavily on East Asian processing despite diverse mining locations.

- The study challenges the belief in diversified mineral supply chains and recommends metal-specific strategies including expanding processing outside dominant regions, strengthening existing diversity, and increasing recycling to reduce dependence on concentrated suppliers.

A 2026 study led by Ramsha Akhter and colleagues at the University of Texas at Arlington, published in Commodities, offers a clear, data-driven look at who controls the supply of six critical battery metals: lithium, cobalt, nickel, manganese, copper, and aluminum. By combining U.S. Geological Survey data, company reports, and Bloomberg analytics, the researchers built a 2024 snapshot of global production by country and by company. Their main finding is simple but important: while mining takes place in many regions, real control is increasingly concentrated in a small number of companies and processing hubs—especially in East Asia. This creates hidden risks across the global energy transition.

Study Methods: Making Sense of a Complex System

The team created two layers of data: total production by country and production by individual companies. They then aligned these datasets using clear rules for ownership, joint ventures, and reporting differences.

To measure the concentration of each market, they used the Herfindahl–Hirschman Index (HHI), a standard economic tool. They also mapped where companies mine materials and where those materials are sent for processing.

When detailed mine-level data were unavailable, the researchers used reasonable estimation methods. This improves coverage but also introduces some uncertainty.

Key Findings: Concentration Drives Risk

The results show that not all metals are equal in terms of supply risk:

- Highly concentrated supply chains

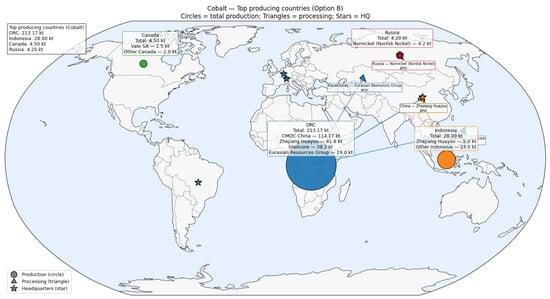

- Cobalt: dominated by mining in the Democratic Republic of the Congo and refining in China

Manganese: controlled by a small number of companies in countries like South Africa and Gabon

- Cobalt: dominated by mining in the Democratic Republic of the Congo and refining in China

- Moderately concentrated

- Lithium and nickel: production is expanding globally, but a few companies still control large shares

- More distributed—but still vulnerable

- Copper and aluminum: mined in many countries, but much of the refining happens in East Asia

The most important takeaway: processing and refining (“midstream”) is the real bottleneck—not mining. Even if raw materials come from many places, they often depend on a few locations for final processing.

Global Cobalt Flows

Implications: Hidden Weak Points in the Energy Transition

For investors and policymakers, the findings highlight several risks:

- Fragile supply chains: disruptions in key regions like China or the DRC could ripple worldwide

- Concentrated power: a small number of firms influence supply, pricing, and access

- Policy gaps: Focusing only on mining does not solve the real problem

The study suggests different strategies depending on the metal:

- Strengthen existing diversity (copper, aluminum)

- Expand processing outside dominant regions (lithium, nickel)

- Reduce dependence through recycling or substitutes (cobalt, manganese)

Limitations: Important but Not Perfect

The study is strong, but not complete:

- It relies partly on company disclosures, which may be incomplete

- Smaller producers are not fully included, which could slightly understate concentration

- Some national production data were adjusted to match company reports

These factors introduce uncertainty. They also point to a larger issue: global mineral data remains neither fully transparent nor consistent.

Bottom Line: The Illusion of Diversity

This study challenges a common belief that global mineral supply chains are well diversified. In reality, control is becoming more concentrated—especially in processing. The future of energy depends not just on where minerals are mined, but on who refines them and where that refining happens. Until that bottleneck is addressed, supply chain resilience will remain more promise than reality.

Citation: Akhter, R. et al. (2026). Mapping the Supply Chain of Lithium-Ion Battery Metals from Mine to Primary Processing by Country and Corporation. Commodities, 5(1):2.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →