Highlights

- Saudi Arabia's Manara Minerals is pivoting from acquiring minority stakes in overseas mines to structured deals including joint ventures, debt investments, and supply arrangements—prioritizing capital efficiency and domestic value-chain control over asset ownership.

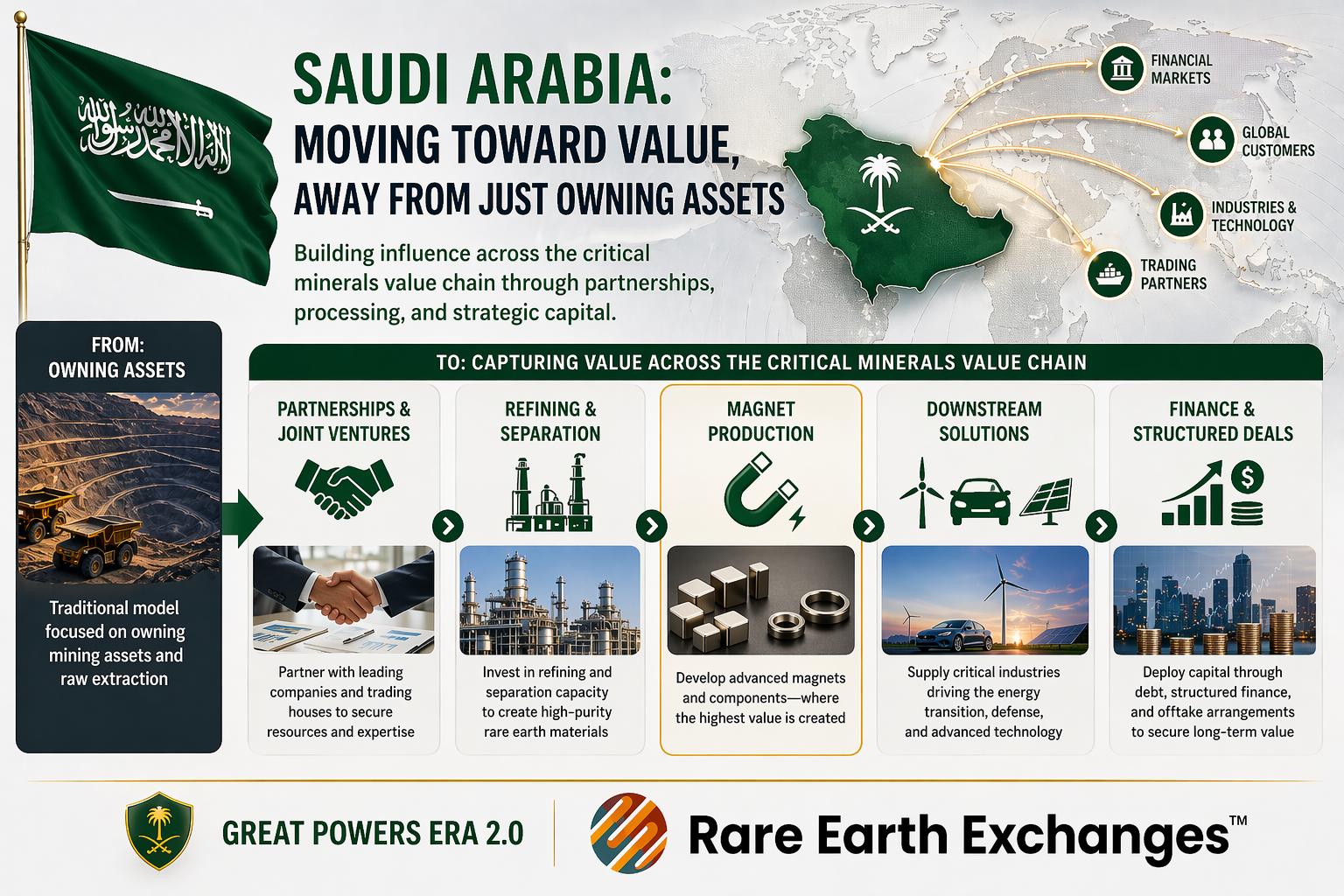

- This shift reflects Great Powers Era 2.0 logic: Saudi Arabia aims to control critical mineral flows through processing, financing, and offtake agreements rather than owning ore bodies, building domestic industrial depth with partners like MP Materials and Ma'aden.

- While years away from rare earth dominance, Saudi Arabia's combination of PIF capital, Ma'aden's operating backbone, and strategic partnerships positions the kingdom as a serious long-term entrant capable of reshaping global critical mineral value chains through persistent investment and node control.

A recent Bloomberg account (opens in a new tab) suggests Saudi Arabia’s Manara Minerals Investment Co (opens in a new tab). is moving away from the strategy it was created for: taking minority stakes in overseas mines and funneling feedstock back into the kingdom. Instead, it is now leaning toward joint ventures with trading houses, debt investments, and supply arrangements tied to future output, with pure equity no longer the primary instrument. If the shorthand is “JVs and structured deals instead of buying equity,” that is directionally correct.

So what are the implications? Saudi Arabia used to plan to buy parts of mines in other countries. Now, it is changing its approach. Instead of owning those mines, it wants to partner with companies, lend money, or make deals to get the minerals it needs later. This lets them secure resources without spending as much money buying the mines themselves.

What makes this important is that it does not look like a retreat from critical minerals. It looks like a retooling. The updated approach is more about securing flows, processing, and optionality than about owning ore bodies abroad.

In practice, that means using capital to lock in supply and build domestic industrial depth inside Saudi Arabia rather than tying up large amounts of money in minority stakes overseas. That logic also fits the kingdom’s broader April 15, 2026 shift toward a more domestically weighted investment posture per the piece authored by Dinesh Nair, Thomas Biesheuvel, and Archie Hunter at Bloomberg.

Tracking the Train

The contrast with the original design is stark. Manara was launched by the Saudi Public Investment Fund (PIF) and Ma'aden to acquire overseas exposure to strategic minerals, and its marquee deal was the roughly $2.5 billion purchase of a 10% stake in Vale Base (opens in a new tab) Metals.

But by January 2026, Saudi officials were already saying the vehicle needed to evolve from a pure investment platform into one with greater technical capability. Now the most recent reporting emphasizes this evolution has moved from concept to operating strategy.

Rare Earth Exchanges™ reviewed this unfolding dynamic with interest. By January 14, 2026, Saudi mining minister Bandar Al-Khorayef said PIF planned to spin off Manara in order to sharpen its focus and add technical capability. That matters because it is effectively an official acknowledgment that a sovereign balance sheet is not the same thing as mining know-how.

And despite bids for assets in Africa and Asia, Manara had completed only one major transaction so far: the Vale Base Metals stake.

PIF’s new five-year plan shifts the sovereign fund toward an 80% domestic and 20% international allocation, down from a peak international weighting of 30%. Saudi officials had been stepping away from expensive projects with weak returns and were focusing more explicitly on revenue generation and domestic economic transformation.

And this wider reprioritization we review lines up almost perfectly with Bloomberg’s portrayal of Manara becoming more capital-efficient and more domestically useful.

Also, PIF publicly described its mining ambition as extending “far beyond extraction,” emphasizing the full value chain from exploration and mining to downstream processing, refining, and end-product manufacturing. That statement is important because it shows the domestic-value-chain logic predates the latest news on this topic; the current shift is less a sudden reversal than the logical next step in a strategy that already prioritized industrial depth inside the kingdom.

Of course, by May 2025, MP Materials and Maaden announced an agreement to explore a vertically integrated rare-earths chain in Saudi Arabia covering mining, separation, refining, and magnet production. And it is exactly this kind of model that the latest news suggests Manara prefers: not just owning upstream assets, but partnering with technical operators to build downstream capability in the kingdom.

By November 2025, Maaden then moved from a memorandum to a binding term sheet, announcing a rare-earth refining and separation joint venture in Saudi Arabia with MP Materials, with Maaden holding at least 51%. That is a concrete example of the new playbook: bring in technical expertise, keep strategic control, build processing at home, and use Saudi Arabia as the hub for value-added activity.

Great Powers Era 2.0

The shift by Manara away from outright mine ownership toward joint ventures, financing, and supply-linked deals is a textbook example of what Rare Earth Exchanges has framed as Great Powers Era 2.0—where control over supply chains matters more than ownership of assets. In this model, countries like Saudi Arabia are not trying to buy the world’s mines outright; they are positioning themselves at the critical nodes—financing, processing, and offtake—where leverage is highest.

Importantly, this reflects a broader geopolitical shift: power is no longer defined simply by resource endowment or capital deployment, but by the ability to shape flows, dictate terms, and secure access across the value chain. In that sense, Saudi Arabia’s strategy is not a retreat from global mining—it is a more sophisticated play to control outcomes without owning everything, aligning precisely with the REEx thesis that in this new era, “alignment is not control—but access, influence, and positioning are.”

Other Data Points

Two additional official signals deepen the picture. On November 19, 2025, Saudi Arabia’s Ministry of Industry and Mineral Resources (opens in a new tab) said Vedanta’s planned copper rod plant in Ras Al Khair would help build a copper value chain “from mining to final production,” explicitly stating that the ministry wants investors who add value beyond extraction. And on February 1, 2026, the same ministry launched EEP Wave 3 (Exploration Enablement Program, Wave 3), offering up to 25% cash incentives on eligible exploration spend plus salary support, which is another way of saying the kingdom is willing to subsidize the upstream pipeline needed to feed domestic processing later on.

Why Riyadh Changing Course?

The first reason is capital discipline. Per the Bloomberg (and others) piece, Manara had struggled to find deals at attractive valuations and is now pursuing more capital-efficient structures. Importantly, PIF has shifted toward heavier domestic deployment and sharper return discipline. Put differently, the kingdom seems less interested in paying full price for minority stakes in other people’s mines and more interested in structures that secure supply without consuming as much equity capital.

The second reason is capability. Al-Khorayef told Reuters that the point of spinning off Manara was to shift the culture from a pure investment vehicle to one with greater technical capability, explicitly noting that PIF is a large investor but does not itself possess mining expertise. That is unusually revealing. It suggests Saudi policymakers themselves see the problem the user flagged: money alone is not enough in mining, especially in complex value chains like rare earths.

The third reason is that the Saudi strategy increasingly looks like an integrated industrial strategy rather than a portfolio strategy. The most useful outside framing comes from a December 2025 analysis (opens in a new tab) by the Arab Gulf States Institute (opens in a new tab), which argued that Saudi Arabia is trying to build an integrated mining sector while some neighboring Gulf states rely more on selective overseas financial exposure. That distinction fits the evidence well: Saudi Arabia is not just trying to gain exposure to critical minerals prices; it is trying to assemble exploration, feedstock, processing, logistics, and downstream manufacturing into one national platform.

NewModels Unfolding?

The emerging Saudi model has four moving parts based on an extensive Rare Earth Exchanges review. First, de-risk exploration domestically through licensing rounds, geological data, and direct incentives. Second, secure feedstock and optionality through JVs, trading partnerships, and offtake-linked credit rather than relying mostly on equity ownership. Third, anchor higher-value stages such as separation, refining, and possibly magnets in Saudi Arabia itself. Fourth, use foreign partners for the expertise that Saudi entities do not yet fully possess.

In that sense, Saudi Arabia appears to be trading asset ownership for platform control. That is an inference, but it is a well-supported one. If Manara lends to miners in exchange for offtake rights, if Maaden runs the domestic processing hub, if the ministry subsidizes exploration, and if foreign partners bring technology and process knowledge, the kingdom can shape a large part of the value chain without having to own every mine. For rare earths in particular, that could be a very rational move because separation, refining, qualification, and customer relationships are where strategic bottlenecks often sit.

From Capital to Control: Saudi Scale Meets Hancock Execution

On financial firepower, Saudi Arabia is formidable. Backed again by PIF and aligned national policy, the kingdom can deploy capital at a scale few private actors can match. If the contest centers on securing feedstock, financing refineries, or structuring offtake agreements, the Saudi model direction is powerful—designed to control flows rather than simply own assets. But this is not just a story of capital. Through Ma'aden, Saudi Arabia brings an operating backbone—an established mining company with global reach. Still, Saudi officials themselves have acknowledged a gap: sovereign capital is not the same as deep technical mining expertise, and that capability must be built or acquired.

That is where Hancock Prospecting’s (opens in a new tab) edge is unmistakable. It operates at scale, moving tens of millions of tonnes of ore annually through integrated infrastructure it owns and controls. More importantly, led by Australia’s wealthiest woman, Gina Rinehart, the investment group has assembled a strategically coherent rare earths portfolio—stakes in Lynas Rare Earths, MP Materials, and Arafura Rare Earths—anchoring it in the core of the non-China supply chain. This is execution: geology, logistics, development, and timing. It reflects not just capital, but decades of operating rhythm and decision-making under real market conditions.

Yet the dynamic is more complex than competition. In Saudi Arabia itself, Ma’aden and Hancock are already partners, not adversaries—working jointly to accelerate exploration. That points to the real outcome: coopetition. Saudi Arabia is positioning itself as a global hub for financing, processing, and downstream value capture, while leveraging partners like Hancock for upstream expertise. This aligns directly with the Rare Earth Exchanges Great Powers Era 2.0 thesis—power lies not in owning everything, but in controlling key nodes of the system. The real question is whether Saudi Arabia can absorb enough expertise, fast enough, to convert financial strength into lasting industrial advantage.

Could the Saudi’s at some point ultimately compete with, say, a Hancock Prospecting? Yes, especially as a hub-builder and capital provider. But the more precise answer is that Saudi Arabia may become strongest where Hancock is relatively less dominant: structured financing, domestic processing build-out, policy coordination, and supply-chain orchestration. And note, recently, REEx John Parkinson issued recommendations to Hancock covering some of these topics.

Investor Note

Saudi Arabia is years—likely a decade or more—away from becoming a true rare earth superpower. The technical barriers are substantial: solvent extraction at scale, heavy rare earth separation, product qualification, and integration into global magnet supply chains are complex, time-intensive processes. These are not capabilities that can be built overnight, regardless of capital.

That said, investors should not dismiss the trajectory. Backed by the Public Investment Fund, anchored by Ma'aden, and supported by a growing network of global partnerships, Saudi Arabia brings a powerful combination of capital, industrial discipline (honed in oil refining), and state coordination. This positions the kingdom not as an immediate competitor to established players, but as a serious long-term entrant capable of reshaping parts of the value chain.

The implication is straightforward: this is not a near-term disruption story—it is a slow-build strategic shift. Markets may underprice this today, but over time, Saudi Arabia’s ability to move upstream—particularly into processing, refining, and downstream integration—should be taken seriously. In the context of the Rare Earth Exchanges Great Powers Era 2.0 thesis, this is exactly how newpower centers emerge: not through speed, but through persistent capital deployment, partnerships, and control of critical nodes.

0 Comments