Highlights

- China's rare earth price index closed at 265.1 on May 15, 2026, down from early-2026 highs above 300, with heavy rare earths showing modest domestic price declines despite their increasing strategic value to Western defense and technology sectors.

- A striking market paradox emerges: heavy rare earths like dysprosium and terbium are weakening in China's controlled domestic market while ex-China buyers reportedly pay multiples several times higher to secure non-Chinese supply, signaling the emergence of two partially decoupled rare earth markets.

- Chinese rare earth pricing reflects state industrial policy rather than pure market forces, while the fragmented ex-China market remains opaque with bilateral contracts and uncertain pricing floors, making rare earth prices increasingly signals of geopolitical leverage rather than simple commodity indicators.

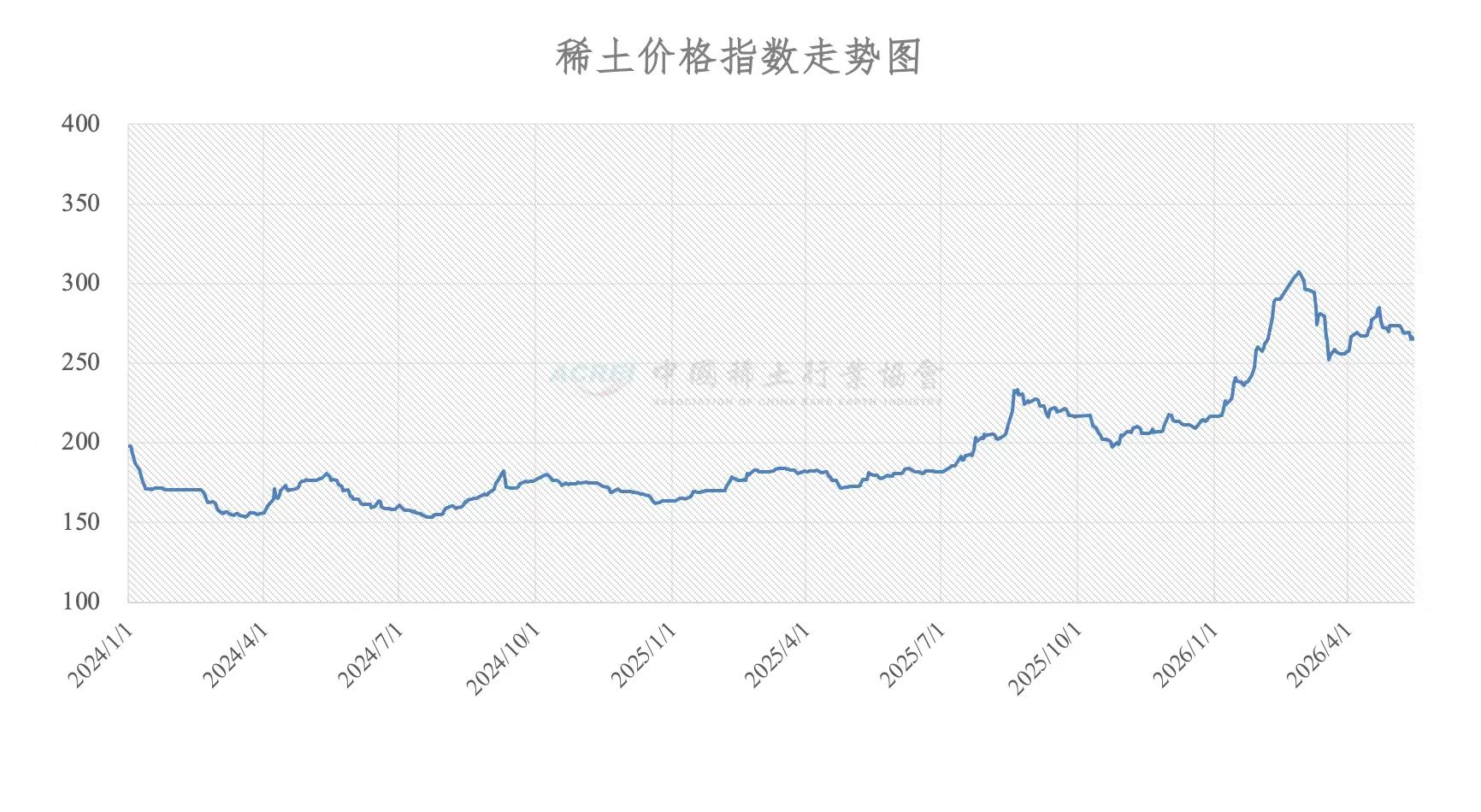

China’s official rare earth price index closed at 265.1 on May 15, 2026, according to the China Rare Earth Industry Association, remaining far above its 2010 baseline of 100 even after retreating from early-2026 highs above 300. The message from Beijing’s domestic market is subtle but important: prices remain historically elevated, yet the market no longer appears to be in acute stress mode despite intensifying geopolitical competition over critical minerals.

For Western investors, however, the more important signal may be what is happening beneath the surface. China’s most strategically important heavy rare earth elements—essential for high-temperature permanent magnets used in EV drivetrains, missiles, drones, robotics, wind turbines, and advanced defense systems—are showing mild weakness domestically even as ex-China buyers increasingly treat them as scarce strategic assets.

The Heavy Rare Earth Paradox

The latest pricing table shows many light rare earth products broadly stable, while several heavy rare earth categories were marked “跌” (“down”), indicating modest price declines. Using an approximate conversion rate of ¥1 = $0.15 USD, key reference prices included:

- NdPr Oxide: ¥728.2–748.2/kg ≈ $109.23–$112.23/kg

- Dysprosium Oxide: ¥1,305–1,345/kg ≈ $195.75–$201.75/kg

- Terbium Oxide: ¥6,065–6,125/kg ≈ $909.75–$918.75/kg

- Gadolinium Oxide: ¥167–187/kg ≈ $25.05–$28.05/kg

- Holmium Oxide: ¥500–520/kg ≈ $75.00–$78.00/kg

This creates a striking paradox. Heavy rare earths are arguably becoming increasingly strategically valuable to the West, with ex-China buyers reportedly willing to pay multiples of domestic Chinese reference levels to secure non-China supply. Yet inside China, prices remain relatively contained.

That divergence increasingly suggests the emergence of two partially decoupled rare earth markets.

China still possesses scale advantages the West lacks: dominant refining capacity, internal inventories, export controls, quota systems, vertically integrated magnet manufacturing, and substantial state influence across the supply chain. Western markets, by contrast, are driven by urgency: defense procurement concerns, qualification bottlenecks, fragile supply diversification efforts, and limited heavy-rare-earth separation capacity outside China.

The Pricing Mirage

Investors should avoid treating Chinese rare earth prices as pure free-market discovery mechanisms. China’s market is deeply influenced by industrial policy, state coordination, environmental regulation, export licensing, strategic stockpiling, and national security priorities. China state-owned or supported rare earth enterprises can be seen as tools of state industrial policy.

The so-called ex-China market is also far from transparent. Because roughly 90% of global rare-earth refining still occurs in China (98% or so of heavy rare-earth elements), non-China pricing remains fragmented and immature. Most transactions occur through bilateral contracts with confidential terms, qualification requirements, tolling structures, and long-term strategic supply arrangements. Pricing agencies capture only partial snapshots of a largely opaque market.

The MP Materials Floor Question

One increasingly important psychological benchmark is the reported $110/kg NdPr floor framework associated with the U.S.-supported arrangement involving MP Materials (Australia has established the floor as well). Some market participants now assume this effectively establishes a Western pricing floor.

That assumption may prove premature.

There is still insufficient evidence that comparable pricing structures have spread broadly across the wider ex-China rare-earth market.

Bottom Line

Rare-earth prices are no longer just commodity signals. They are increasingly signals of industrial power, geopolitical leverage, and supply-chain control.

Disclaimer: This report relies primarily on pricing information published by the China Rare Earth Industry Association, a state-linked Chinese industry body. Pricing data should be independently verified through commercial intelligence, bilateral contract data, and third-party market sources.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →