Highlights

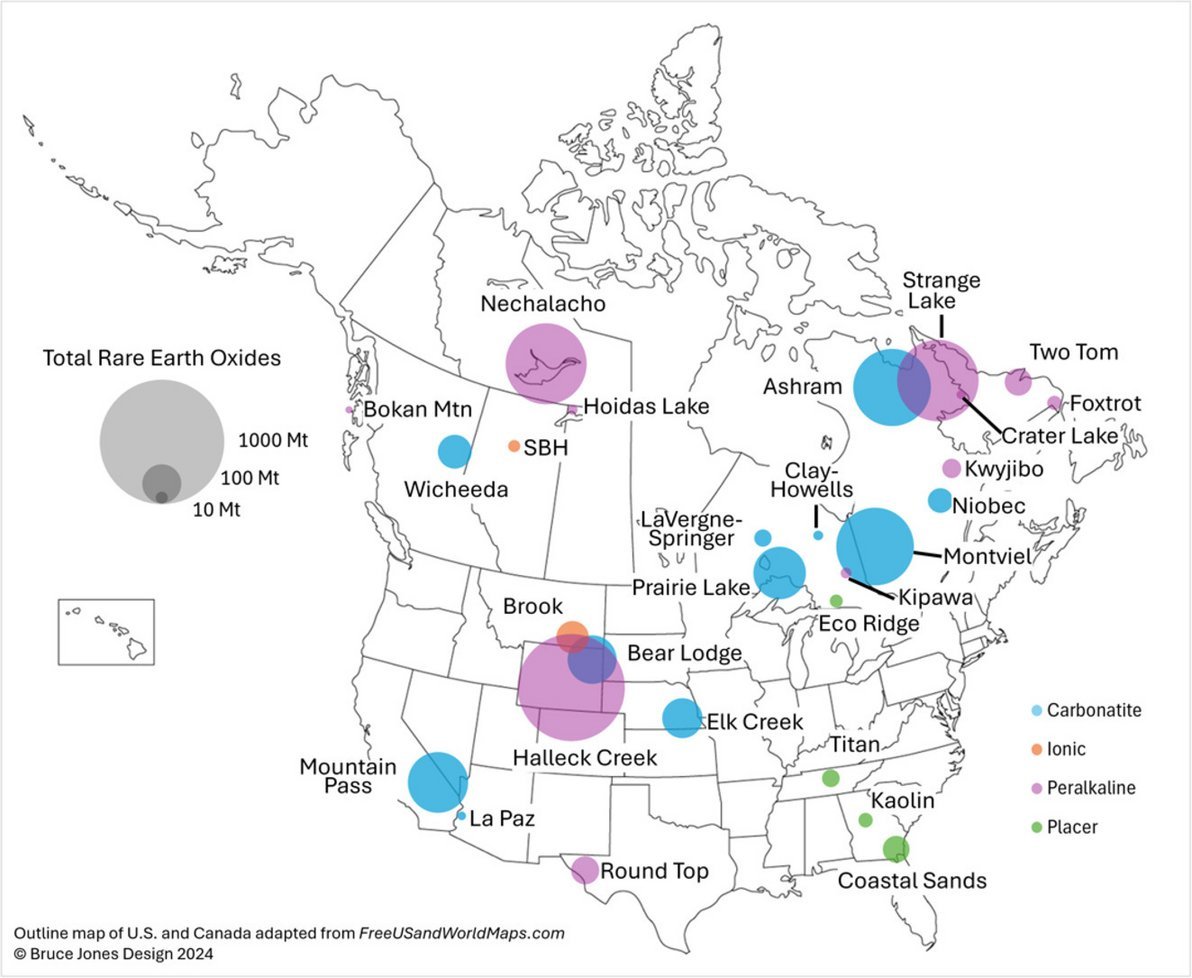

- University of Michigan-led study identifies 28 North American deposits with ~35 million tonnes of total rare earth oxides, roughly 90 times annual global production.

- Mountain Pass, Bear Lodge, Wicheeda, Strange Lake, and Nechalacho are highlighted as key future contributors, with Canadian alkaline deposits offering strong heavy rare earth potential.

- Experts warn that resource size is only the starting point—mineralogy, processing, separation, and policy support all determine whether deposits become viable producers.

- The study is a geological assessment, not a commercialization roadmap; it does not model capital costs, permitting timelines, metallurgical recoveries, or mine-to-magnet economics.

- Replicating China's rare earth ecosystem requires coordinated investment across mining, separation, alloy production, and magnets—not just mine development.

North America possesses enough identified rare earth resources to significantly reduce its dependence on foreign supplies, according to lead author Stephen Kesler (opens in a new tab) and colleagues from the University of Michigan, Ford Motor Company, and collaborating institutions. Published in Resources, Conservation & Recycling, the study (opens in a new tab) identifies 28 drill-tested deposits across the United States and Canada containing an estimated 35 million tonnes of total rare earth oxides (TREO)—roughly 90 times current annual global production. Yet the authors caution that geology alone cannot create a secure supply chain. Bringing these resources to market will require sustained investment in mining, processing, infrastructure, and industrial policy.

Source: Resources, Conservation and Recycling

REEx Evidence Strength Rating: 8.5/10 (Strong). The geological analysis is comprehensive and well-supported, but the pathway from resource to commercial production remains highly uncertain. In this way, the study should not be misunderstood as an assessment of the viability of a commercial industry in the short run.

The researchers analyzed publicly available NI 43-101 and JORC technical reports covering ore grades, tonnage, mineralogy, heavy versus light rare earth distributions, mining methods, processing characteristics, and environmental considerations including thorium management. They then benchmarked North American deposits against major rare earth projects in China, Australia, Greenland, and elsewhere to assess their relative commercial potential.

Findings

The results reveal both opportunity and complexity. Mountain Pass remains North America's premier producing mine, but the study identifies several additional deposits—including Bear Lodge, Wicheeda, Ashram, Strange Lake, Nechalacho, Halleck Creek, and Round Top—as potential contributors to future supply. The authors also highlight Atlantic Coastal Plain heavy mineral sands and Georgia kaolin tailings as potentially faster, lower-capital sources of incremental production because they could leverage existing mining operations.

Importantly, they conclude that Canada's alkaline deposits—particularly Strange Lake and Nechalacho—may offer the continent's strongest long-term heavy rare earth potential, while cooperative U.S.-Canadian development could improve continental supply resilience.

Reality Takes

From Rare Earth Exchanges®' perspective, however, the paper highlights a reality often overlooked in public discussion: a rare earth resource is not a rare earth supply chain.

Resource size and grade represent only the starting point. Mineralogy determines beneficiation. Beneficiation determines hydrometallurgical recovery. Recovery determines separation economics. Separation enables metal making, alloy production, permanent magnet manufacturing, and ultimately commercial qualification by downstream customers. Every step introduces technical, financial, regulatory, and timing risks that can dramatically alter project economics. Two deposits with similar TREO grades can produce vastly different commercial outcomes once recovery rates, impurities, radioactive waste handling, reagent consumption, and capital costs are considered.

Unfolding Assumptions

The study also assumes continued government support for domestic supply-chain development. That assumption deserves scrutiny. China's leadership was built not simply through abundant resources, but through decades of coordinated investment across mining, separation, metal production, alloy manufacturing, permanent magnets, technical talent, and downstream industrial demand. Replicating that ecosystem will require sustained policy support extending well beyond mine development.

The principal limitation is that this is fundamentally a geological resource assessment, not a commercialization study. It does not model detailed process flowsheets, metallurgical recoveries, solvent extraction performance, capital intensity, permitting timelines, customer qualification, financing constraints, or mine-to-magnet economics. Nor does it fully evaluate market dynamics, including pricing volatility, feedstock qualification, or competition from established Chinese processors. Those factors—not resource size alone—determine which North American deposits become commercially viable producers, and an estimate as to how much it will take in expertise and milestones.

Citation: Kesler S., Keoleian G., Hitt C., Cieply J., Kim H.C., De Kleine R., Anderson J.E. Onshoring North American Rare Earth Mining. Resources, Conservation & Recycling. 2026;234:109027. DOI:10.1016/j.resconrec.2026.109027.

Register today: REEx Marketplace™ (opens in a new tab)

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →