Highlights

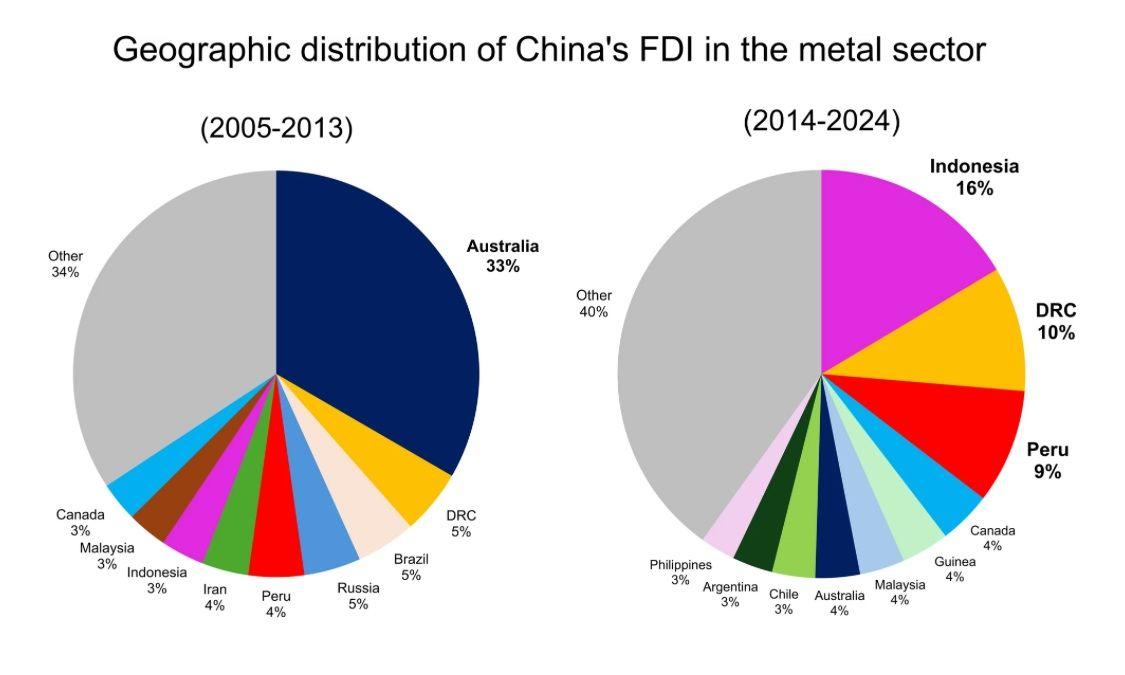

- Chinese FDI in metals shifted dramatically after 2014: Australia’s share dropped from 33% to 4%, while Indonesia, the DRC, and Peru saw surges targeting battery-critical minerals like nickel, cobalt, and lithium.

- This rebalancing aligns with China’s electric vehicle and renewable energy ambitions, moving beyond bulk commodity security to construct integrated supply networks for strategic technologies.

- The study reveals China now bundles mining investments with infrastructure projects, creating economic interdependence while exposing Western supply chain vulnerabilities in critical minerals.

A new study (opens in a new tab) by Joseph Le Bihan, José Halloy, Sabina Issehnane, and Florian Vidal (PEPR research program, France) analyzes nearly twenty years of Chinese foreign direct investment (FDI) in the global metal sector and identifies a decisive strategic realignment. Comparing 2005–2013 with 2014–2024, the authors document a clear shift away from large-scale investments in Australia’s iron ore and bauxite toward targeted stakes in battery and technology-critical minerals in Indonesia, the Democratic Republic of Congo (DRC), Peru, Guinea, Chile, and Argentina. The study argues that this rebalancing coincides with China’s industrial upgrading in the 2010s, the expansion of electric vehicles and renewable energy systems, and the rollout of the Belt and Road Initiative (BRI). In plain terms: China is no longer prioritizing bulk commodity security alone—it is constructing a globally integrated supply network to anchor dominance in strategic technologies.

Study Methods: Data Meets Strategy

The authors combine quantitative FDI flow data from 2005–2024 with qualitative geopolitical and policy analysis. They examine capital allocation patterns, mineral specialization by host country, and linkages between mining investment and parallel infrastructure projects. A focused case study of Peru illustrates how Chinese mining investments often coincide with transport corridors, port development, and energy infrastructure—embedding mineral extraction within broader economic integration strategies.

Key Findings: A Structural Geographic Rebalance

During 2005–2013, Australia accounted for 33% of Chinese metal-sector FDI, totaling approximately $35.2 billion. In the 2014–2024 period, Australia’s share fell sharply to 4%, with flows declining to $4.2 billion. The authors attribute this drop to heightened national security scrutiny and rising geopolitical tensions, particularly in the context of Australia’s closer alignment with the United States.

At thesame time, capital surged into resource-rich emergingeconomies:

- Indonesia (16%): Investment rose nearly fivefold—from $3.66 billion to $20.6 billion—focused primarily on nickel and cobalt, critical for lithium-ion batteries.

- DRC (10%): Increased flows targeted cobalt, copper, niobium, and tantalum—minerals central to energy storage and electronics.

- Peru (9%): Copper investments more than doubled.

- Guinea (aluminum) and Chile/Argentina (lithium) also experienced meaningful growth.

The post-2014 portfolio is more diversified but also more specialized, concentrating on countries with high market concentration of specific strategic minerals. Investments increasingly bundle mining with energy and transport infrastructure, reinforcing long-term economic interdependence.

Implications: From Bulk Metals to Battery Strategy

The findings mark a transition from traditional base metals toward batteryand energy-transition materials. This aligns with China’s ambitionto lead in electric vehicles, grid storage, renewables, and advanced electronics. Securing upstream mineral reserves strengthens downstream advantages in refining, manufacturing, and export markets—where China already commands significant capacity.

For Europe and North America, the study underscores structural exposure in critical mineral supply chains. Policy responses may need to include expanded recycling, processing capacity, allied resource partnerships, and coordinated industrial strategy.

Limitations and Contested Interpretations

The analysis centers on formal FDI flows and may not fully capture complex joint ventures, state-backed financing mechanisms, or informal strategic influence. It does not deeply evaluate environmental governance or laborstandards in host nations. Critics argue such concentrated investmentcan create economic dependency or geopolitical leverage; proponents contend that infrastructure development and capital inflows accelerate host-country growth.

Conclusion

China’s overseas mining strategy has evolved from volume-driven resource acquisition toward targeted control of strategic mineral nodes. This recalibration strengthens its position in global technology value chains while intensifying competition over battery metals and critical materials. The central question now is whether Western economies will proactively build resilient, diversified mineral systems—or continue to respond after strategic ground has already shifted.

Citation: LeBihan, J., Halloy, J., Issehnane, S., & Vidal, F. (2024). Where does China invest abroad in metals and minerals? PEPR Research Program.

2 Comments

2 replies

Loading new replies...

New member

Administrator

Join the full discussion at the Rare Earth Exchanges Forum →