Highlights

- REEx analyzes the Federal Critical Minerals Ecosystem map as proof of policy intensity but warns that institutional density is being confused with industrial capability—financing tools like Project Vault and OSC loans can stabilize demand but leave decisive bottlenecks in heavy rare earth separation, workforce, and permitting largely unsolved.

- The U.S. has deployed four real levers—capital (EXIM's $10B Project Vault, DoD's Office of Strategic Capital), rules (permitting reform gaps), targeting (directed buildout), and diplomacy (FORGE replacing MSP)—yet coordination does not equal throughput when separation chemistry, qualification cycles, and trained metallurgists remain scarce.

- REEx's forecast places credible 50% U.S. magnet resilience in the early 2040s, not 2030, because the federal ecosystem is building a formidable finance-and-policy machine while the unglamorous physics of industrial civilization—purity, yield, repeatability, qualification—remain unscaled outside China.

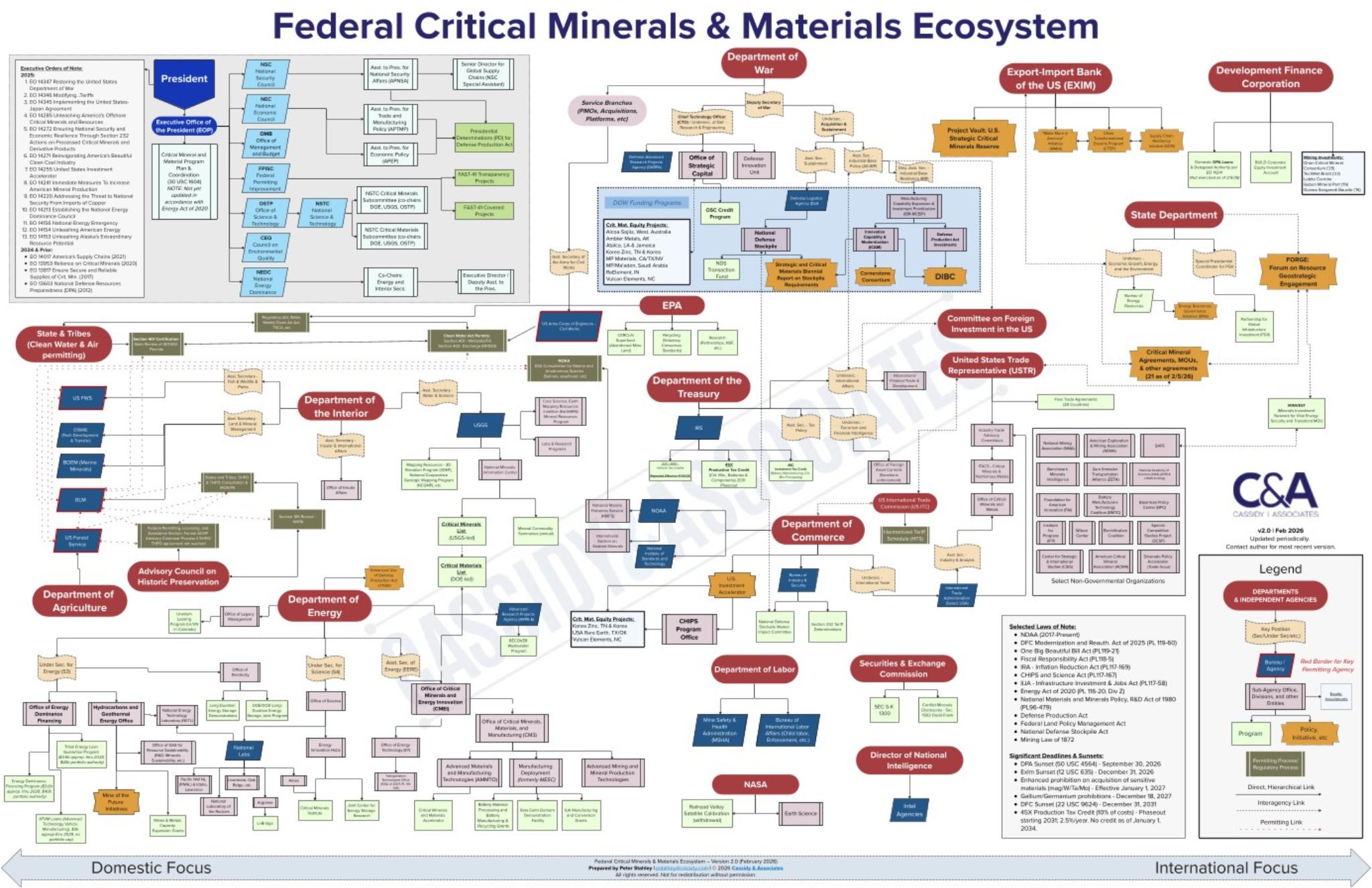

Rare Earth Exchanges review a “Federal Critical Minerals & Materials Ecosystem” map as both proof of U.S. policy intensity and a diagnostic of structural weakness: institutional density is being confused with industrial capability. We translate the sprawl evidenced in an organization schematic uploaded by Peter Stahley into four reallevers—capital, rules, targeting, and diplomacy—then testwhether those levers actually move the mine-to-magnet bottlenecks that matter, especially heavy rare earth separation, workforce, qualification cycles, and permitting throughput. We stress-test Project Vault, FORGE, and DoD’s Office of Strategic Capital as powerful financial and procurement tools that can stabilize demand and de-risk projects—while still leaving the decisive chemistry-and-execution constraints largely intact.

Source: Peter Stahley: Cassady & Associates

The Org Chart as a Rorschach Test

The updated “Federal Critical Minerals & Materials Ecosystem” (credited on the image to Cassady & Associates, v2.0 Feb 2026) is the kind of diagram that makes Washington feel productive: each box a promise, each dotted line a reassurance, each acronym a claim that the machine is finally awake.

And yet geology hasn’t changed. Solvent extraction chemistry hasn’t gotten easier. Qualification cycles didn’t shrink because someone drew an interagency connector.

So what is this map, really?

It is the visual proof of political intensity—and the visual proof of coordination risk.

In a sane world, an ecosystem map would describe a supply chain. In the modern American state, it often describes something else: how many ways a project can be delayed while everyone insists it’s being accelerated.

The Four Levers Hidden Inside the Sprawl

Strip away color, titles, and symbolism and the federal ecosystem is trying to pull four levers. They are real. They are also unevenly matched to the problem.

1) Money as a weapon

Project Vault (EXIM) is not a rumor; it is a live instrument. EXIM says it approved a direct loan of up to $10 billion to Project Vault to launch a “U.S. Strategic Critical Minerals Reserve,” framed as an independently governed public-private partnership intended to store essential raw materials across U.S. facilities and protect manufacturers during market disruptions.

DoD’s Office of Strategic Capital (OSC) is also now a financing node. DoD announced OSC’s first direct loan to MP Materials—$150 million to add heavy rare earth separation capability at Mountain Pass—and explicitly tiedOSC’s expanded critical minerals loan capacity to the One BigBeautiful Bill Act, describing credit subsidy funding that could support far larger aggregate lending.

OSC also announced a $700M conditional loan commitment with Vulcan Elements and ReElement (majority to Vulcan) to expand NdFeB magnet production and related separation/metallization capacity. And these are a serious advancements compared to past administrations—so we are making progress. For example firms such as ReElement’s bring a patriotic drive to critical minerals and rare earth sovereignty, compelling in the best sense of the word. There is visible passion, disciplined execution, and the entrepreneurial ability to mobilize capital and talent toward a national objective. The ambition is real. The capability is emerging. And yet—there remains a long road between aspiration and durable, scaled impact. It’s stating to happen but our government is not there yet.

The financing is the strongest part of the chart included above. Not because money solves chemistry—because it finally admits a truth: the U.S. is trying to win an industrial war with a capital market that doesn’t finance slow, hazardous, technically fragile projects well.

2) Rules and gatekeeping

Permitting, NEPA-era friction, environmental review, and state/tribal interfaces sit like bedrock beneath the whole diagram. Stahley’s own caption captures the paradox: governance has changed; permitting laws have not. A bureaucracy can create ten new “accelerators” and still be governed by the same bottleneck statute-and-litigation reality.

3) Industrial targeting

DoD’s posture has shifted from “market hoping” toward directed buildout: heavy separation lending, conditional magnet capacity commitments, and a more explicit theory of national security supply chain enforcement.

The chart signals that the federal government is no longer pretending the invisible hand will build a mine-to-magnet system by itself. That’s progress we have acknowledged under Trump 2.0.

But targeting must be paired with execution capacity—people, process control, qualified customers, and non-China inputs—otherwise it becomes a funding headline that doesn’t survive commissioning.

4) Diplomacy replacing naïve globalization

On the “international focus” side, the map highlights FORGE as the successor to MSP. Reporting indicates the Minerals Security Partnership was relaunched as the Forum on Resource Geostrategic Engagement (FORGE), aimed at deepening cooperation on investments and coordination across the critical minerals cycle.

This aligns with REEx’s Great Powers Era 2.0 thesis: polite globalization yields to preferential blocs and supply-chain statecraft, at times with use of various forms of militarization.

But diplomacy cannot substitute for throughput. It can coordinate financing, standards, and offtakes. It cannot conjure heavy-REE separation trains.

That is the skeleton. Now comes the hard part: does this skeleton walk?

A Crowded Cockpit: When “More” Becomes Less

The map’s dominant impression is not unity. It’s overlap—sometimes productive, often parasitic.

1) Too many chefs, too few metallurgists

The decisive scarcity is not meeting invites. It is human capital: solvent extraction operators, hydrometallurgy engineers, QC/QA discipline, and the lived know-how required to keep separation plants stable and repeatable—then survive automotive and defense qualification.

No org chart can fast-track competence.

2) Mission conflict is baked in

EPA is not anti-minerals. It is pro-statute.

DoD is pro-speed.

Treasury is pro-control.

Interior is pro-land + law.

Commerce is pro-industry + trade rules.

Dotted lines don’t dissolve these differences; they just make conflict look collaborative.

3) Coordination does not equal throughput

Interagency processes often increase the number of approvals needed to move, especially when new programs generate new reporting obligations, new review layers, and new “risk governance” rituals that are politically rational but industrially corrosive.

4) The diagram mistakes programs for capacity

A loan facility is not a separate plant.

A stockpile is not a magnet foundry.

A committee is not a trained workforce.

Obvious? Good. The market keeps forgetting.

Project Vault: Strategic Reserve—or Strategic Narrative?

Project Vault is substantial and explicit:EXIM describes up to $10B of financing to establish a Strategic CriticalMinerals Reserve as a public-private partnership, and it publicly lists intended participants (including named OEMs and commodity suppliers/traders).

Critics such as the expert metals trader Rare Earth Observer (opens in a new tab) and others, who asked to remain anonymous, have suggested that Project Vault is not a true national strategic reserve but rather more like a taxpayer-financed “members club” that benefits select corporations and traders without meaningfully stabilizing the rare earth market. Should not a real sovereign reserve act impartially—buying when prices collapse, selling during spikes, and holding standardized, widely usable inventory to protect the national economy?

But Project Vault is portrayed as a public-private warehouse scheme where companies like GM, Stellantis, and Boeing, and traders such as Traxys or Mercuria, commit to future purchases at fixed prices while taxpayers provide the capital and absorb risk. Do these members even use raw, rare-earth products directly? In reality, many require finished magnets, not oxides. Rare earth elements are, in fact, specialty chemical products requiring precise grades—not one-size-fits-all commodities. Is the timing not poor because reserves typically sell into high prices, not buy during uncertainty? We won’t get into the inside expert chatter criticizing U.S. support for what could be deemed weak or technically flawed projects (e.g., unconventional extraction, novel separation technologies, Greenland deposits with problematic mineralogy).

Compared to China’s more mature reserve system and processing dominance, the U.S. approach risks distorting markets, encouraging hoarding, and misallocating capital. Yes, Project Vault is politically loud, but is it structurally serious? Is it more optics than strategy? After all, insiders tell us that without the absolutely necessary deep processing capacity and precise product knowledge, the stockpiling of raw materials will notsecure the downstream magnet supply chain.

Hence, REEx treats it as two truths at once:

What it is (credible)

- A demand backstop and inventory buffer that can reduce panic cycles during disruptions.

- A way to make “criticality” tradable: stored tonnage, contracted access, predictable logistics.

- A signal to miners/refiners that buyers may exist even when pricing gets weaponized.

What it is not (often implied)

- Not a shortcut around heavy-REEseparation bottlenecks. And that’s the real problem—see our recent assessment as to the true timelines for supply chain resilience.

- Not a substitute for downstream qualification.

- Not “ex-China resilience” if stored material still relies on Chinese processing or Chinese-controlled chokepoints.

The uncomfortable question

If a federally enabled reserve becomes the new liquidity center, who gets preferred access, and on what terms? That’s not a conspiracy theory. It is the natural question anytime finance and inventory are centralized around a state-aligned instrument.

FORGE Replaces MSP: Harder Power, Same Bottleneck

The rebrand to FORGE signals a shift from cooperative branding to geostrategic realism—investment coordination, diplomacy, and joint project identification. But again: FORGE can harmonize policy; it cannot manufacture solvent-extraction competence or produce Dy/Tb outside China on a political schedule.

In the Great Powers Era 2.0, bloc diplomacy is necessary. It is not sufficient.

The REEx Reality Check: 2030 Is Political, 2040 Is Industrial

REEx’s own forecast based on the current policies is blunt: under a strict“cutoff scenario” definition, the median timeline for 50%U.S. magnet resilience is the early 2040s, with an 80% confidence band of ~2039–2046—and 50% by 2035 is low probability without far faster heavy rare earth scaling outside China than current evidence supports.

This is not pessimism. It is an engineering timeline. It’s subject to change with more advanced industrial policy and execution.

And the chart—ironically—supports REEx more than it supports the triumphal narrative:

- It shows intensity of action.

- It also shows how much of the action is administrative and financial, not chemical and industrial.

DoD and EXIM can movemoney faster than the United States can commission separation trains and qualify magnet output at scale.

That mismatch is the heart of the problem.

The Core Critique: Institutional Density Is Not Dominance

This map is a useful artifact—but the wrong conclusion is often drawn from it.

What it proves

The U.S. has entered a new phase: more agencies engaged, more authorities used, and capital tools operationalized.

What it does not prove

That the U.S. is on a credible near-term path to mine-to-magnet resilience—because the decisive variables remain:

- heavy-REE separation outside China

- qualified downstream production

- workforce + operating know-how

- permitting throughput

- durable pricing architecture and offtake

REEx’s forecast argues that those remain unsolved at the necessary scale.

A Better Way to Read the Chart

Read it as a crowded control room: too many hands on the dials, too few people in therefinery.

America may be building a formidable finance-and-policy machine. But critical minerals dominance is built on throughput, purity, yield, repeatability, and qualification—the unglamorous physics of industrial civilization.

Until those boxes translate into those outcomes, the “myriad structure” is not a victory parade.

It is a diagram of a nation trying to remember how to make things again.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →