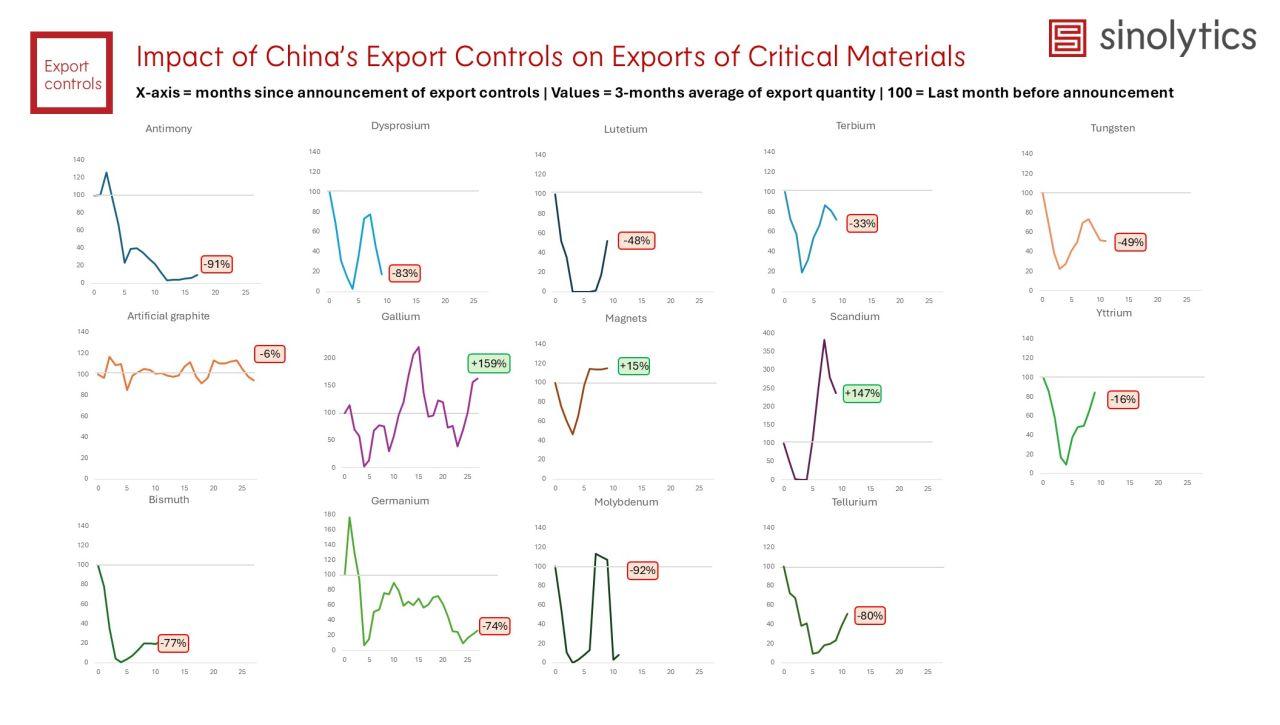

- New export data reveals China's critical minerals controls remain uneven despite pledged relaxations, with antimony (-91%), germanium (-74%), and dysprosium (-83%) showing sustained contractions while gallium (+159%) and scandium (+147%) rebound strongly.

- Implementation varies significantly by material and strategic relevance, suggesting selective rather than blanket controls, with heavy rare earths key to defense and EV supply chains experiencing persistent licensing frictions.

- Policy volatility remains an embedded risk for global supply chains as relaxation rhetoric does not equal normalized trade, requiring diversification strategies beyond reliance on Chinese exports.

New export data suggests that while China has pledged to relax certain export controls introduced last October, the operational reality remains uneven across critical minerals markets. An analysis published by Jost Wübbeke of Sinolytics (opens in a new tab) (Berlin/Beijing) indicates that although some recent measures have been lifted, earlier restrictions continue to shape trade flows. The key issue is not the existence of controls, but how they are implemented.

Source: Sinolytics

According to Sinolytics’ data (3-month rolling averages indexed to pre-control levels), several materials show sustained export contraction. Antimony (-91%), Bismuth (-77%), Germanium (-74%), Tellurium (-80%), and Molybdenum (-92% for selected HS codes) display persistent declines. In rare earth-heavy segments, Dysprosium (-83%) and Lutetium (-48%) remain well below baseline, with Dysprosium’s recent drop particularly sharp.

These figures suggest either continued administrative friction or structural shifts in trade.

However, not all materials are contracting. Gallium (+159%), Scandium (+147%), and Magnets (+15%) show strong rebounds. Yttrium (-16%) and Terbium (-33%) reflect partial recovery patterns. Artificial graphite remains largely flat (-6%), challenging narratives of sweeping export suppression.

What Can We Infer?

Three disciplined observations emerge:

1. Selectivity Over Blanket Controls

The data does not support a uniform embargo narrative. Instead, implementation appears differentiated by material and possibly by downstream strategic relevance.

2. Licensing Frictions Persist

Declines in heavy rare earth elements like Dysprosium and Lutetium—key to high-temperature permanent magnets—remain strategically significant. Even partial constraints can disrupt defense, EV, and wind supply chains.

3. Diversification vs. Restriction

Falling exports may reflect foreign buyers diversifying supply, inventory drawdowns, or substitution—not solely tightened Chinese enforcement. Causality cannot be inferred from trend lines alone.

Critical Reading Required

Sinolytics, a European consultancy specializing in China’s policy-driven economy, frames the issue correctly: implementation is decisive. Yet caution is warranted. Trade data indexed to announcement dates captures “shape,” but not contract renegotiations, stockpiling cycles, or transshipment flows.

For rare earth and critical mineral markets, the signal is mixed. Some strategic materials remain constrained. Others are flowing more freely.

The global takeaway: policy volatility remains embedded risk. Relaxation rhetoric does not equal normalized trade.

Source: Jost Wübbeke (opens in a new tab), Sinolytics (LinkedIn post), February 2026.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →