Highlights

- Africa holds world-class deposits of cobalt, PGMs, and graphite but dominates upstream mining only—not midstream refining or downstream manufacturing where real value and leverage exist.

- China controls over 80% of global rare earth separation and magnet production, processing most African concentrates offshore, creating a strategic bottleneck in the value chain.

- For critical mineral investors, the key signal is tracking processing infrastructure and beneficiation capacity, not just geological endowment—industrial execution determines strategic power.

What of the claims that Africa sits at the center of the global critical minerals race? Using USGS-aligned production data and supply chain analysis, the separation of geological strength from industrial control. For rare earth element (REE) and critical mineral investors, the takeaway is clear: deposits matter — but processing power determines leverage.

Africa Is Central — But Not in Command

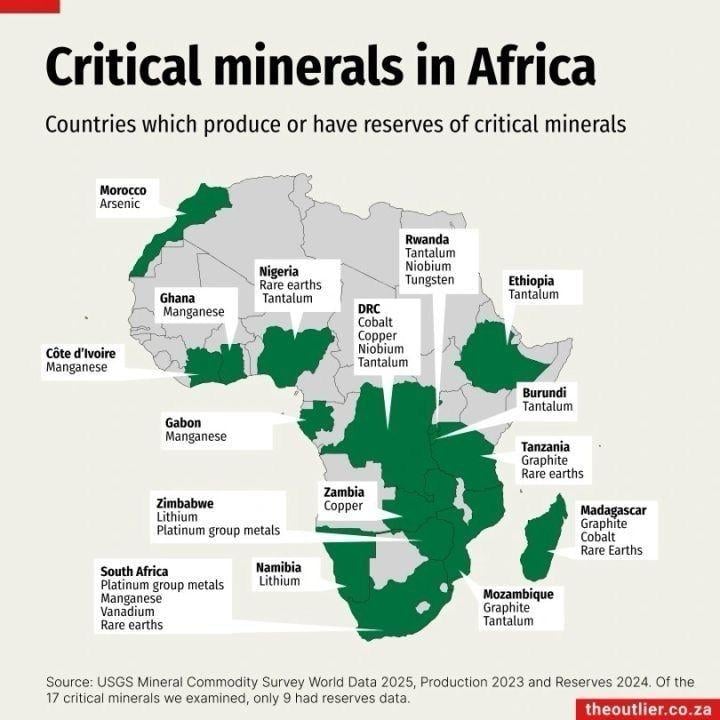

Africa holds world-class deposits of minerals critical to EV batteries, renewables, aerospace, and defense systems. The Democratic Republic of Congo (DRC) accounts for the majority of the global cobalt mine supply. South Africa leads in platinum group metals. Zambia remains a major copper producer. Mozambique and Madagascar are significant graphite suppliers. Zimbabwe and Namibia produce lithium. Tanzania and Madagascar host notable rare earth projects.

These country-mineral pairings above align broadly with U.S. Geological Survey data.

But here is the strategic distinction investors must understand:

Africa dominates segments of upstream mining, not midstream refining or downstream manufacturing. That gap defines power.

Where the Map Is Accurate — and Where It Blurs

The mineral associations shown above are largely credible. However, the graphic blends production, reserves, and exploration-stage assets. These are not equivalent.

For example:

- DRC’s cobalt dominance is established at scale.

- South Africa’s PGM leadership is globally significant.

- Tanzania and Madagascar host advanced rare-earth projects — but Africa does not dominate global REE production.

- Nigeria’s position in rare earths remains early-stage relative to global suppliers.

The geology is strong. The production scale varies widely.

The Value Chain Reality Check

Claims that “Africa dominates critical minerals” require nuance.

Africa leads in cobalt mining and holds major shares in manganese and PGMs. However:

- It does not dominate lithium refining.

- It does not dominate rare earth separation.

- It does not control NdFeB magnet manufacturing.

China retains the overwhelming share of global rare earth separation capacity and magnet production — generally estimated at above 80%. Most African rare earth concentrates are processed outside the continent.

The bottleneck is not ore.

The bottleneck is processing.

The Strategic Inflection Point

The core insight stands: the global contest is shifting from “who owns the minerals” to “who controls the value chain.” Africa’s leverage will expand only if beneficiation, refining, alloying, and advanced manufacturing scale locally. Without that shift, value capture remains offshore.

Then For REE and critical mineral investors, the signal is clear:

Track processing infrastructure, not just resource maps and geological endowment.

So yes, Africa is resource-rich. Yet strategic indispensability depends on industrial execution — not geology alone.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →