Highlights

- Nearly 80% of 39 critical minerals show a dominant producer controlling at least one-third of global output, with China leading in nearly half and holding most monopoly-like positions through industrial capability rather than resource abundance.

- The decisive battleground isn't mining but midstream processing—refining, purification, and separation capacity remain highly centralized in China, particularly for materials like gallium (99%), tungsten (80%+), and silicon (70%+).

- Concentration risk reflects decades of state-backed industrial strategy: those who control processing infrastructure control pricing, timelines, and technological sovereignty in semiconductors, EVs, and defense systems.

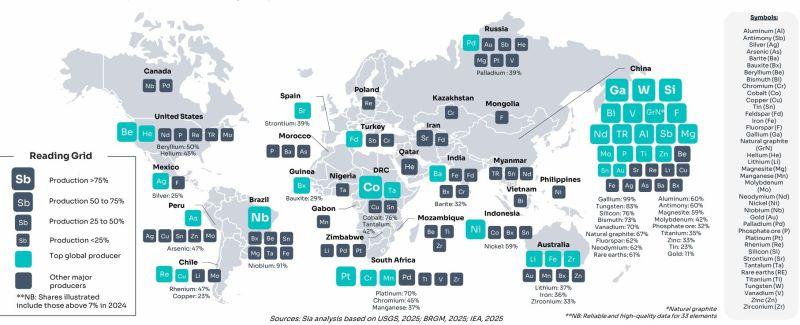

Andrew Chan Yik Hong (opens in a new tab) of the Malaysia Semiconductor Industry Association highlights a structural truth often obscured by reserve maps: production—not geology—defines power. Across 39 critical minerals, nearly 80% show a dominant producer controlling at least one-third of global output, while roughly 25% approach monopoly conditions (>65%). China emerges as the central actor, leading in nearly half of these minerals and anchoring most monopoly-like positions. The implication is clear—industrial capability, not resource abundance, dictates control.

Where the Analysis Holds Firm

Chan’s central thesis aligns with well-established supply chain dynamics. Production concentration is real and persistent. China’s dominance in materials like gallium (99%), tungsten (80%+), and silicon (~70%+) is widely documented and reflects decades of state-backed investment, scale economics, and midstream mastery.

Critically, the post correctly distinguishes reserves vs. production—a gap many policymakers still misunderstand. While resources are globally distributed, processing, refining, and separation capacity are highly centralized, particularly in China. This is especially true in rare earths, where separation—not mining—is the chokepoint.

Where the Argument Needs More Precision

However, the framing leans toward simplification:

- “Monopoly” vs. “Dominance”: A >65% share signals concentration, but not absolute control. Substitution, recycling, and secondary supply (e.g., scrap markets) can soften true monopoly power.

- Static Snapshot Bias: The analysis underweights emerging capacity in Australia, the U.S., and Southeast Asia—particularly in lithium, nickel, and rare earth refining.

- Midstream Undersold: While noted, the post still underemphasizes that refining and magnet manufacturing—not mining—are the decisive battlegrounds.

What’s Actually at Stake

For semiconductors, EVs, and defense systems, this isn’t just a resource story—it’s an industrial systems competition. The ability to process, purify, and manufacture at scale determines who captures value and who bears risk.

Chan is directionally correct: minerals policy is now industrial policy. But the deeper truth is sharper—midstream dominance is geopolitical leverage.

BottomLine for Investors & Policymakers

The map doesn’t show scarcity—it shows concentration risk engineered through industrial strategy. Those who control processing control pricing, timelines, and ultimately, technological sovereignty.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →