Highlights

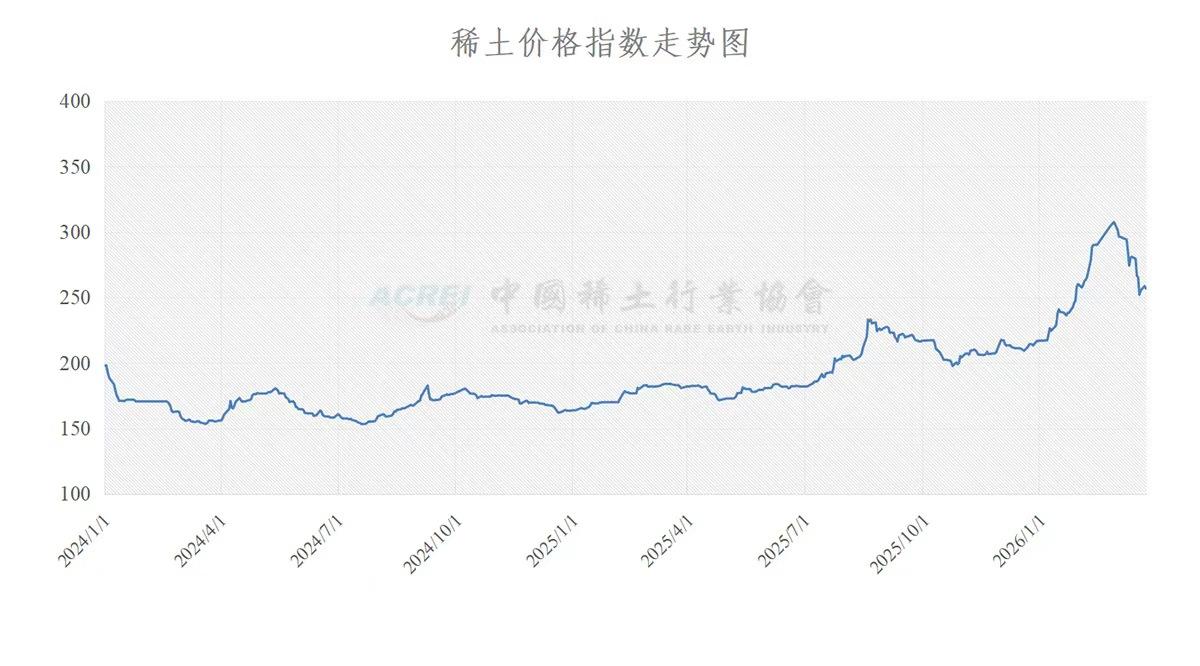

- China's rare earth price index fell to 256.9 on March 24, 2026, down from recent highs above 300, indicating market cooling while prices remain elevated above historical averages with particularly notable declines in magnet-related materials like praseodymium-neodymium compounds.

- The price pullback reflects short-term market recalibration through inventory adjustments and procurement cycles rather than structural breakdown, with most core materials remaining stable while magnet inputs showed selective weakness tied to EV and defense applications.

- Despite near-term price relief, China maintains structural dominance over global rare earth pricing as an ex-China pricing market remains unrealistic due to insufficient processing capacity, limited transaction volumes, and lack of transparent price discovery mechanisms outside Chinese markets.

China’s official rare earth price index registered 256.9 on March 24, 2026, according to the China Rare Earth Industry Association. Prices remain elevated relative to historical levels, while most individual products were reported as stable and a subset—particularly magnet-related materials—showed declines, suggesting short-term softness without altering underlying supply chain dynamics.

The Headline Number: A Pullback, Not a Collapse

The China Rare Earth Industry Association reported the daily rare earth price index at 256.9, calculated using a 2010 baseline of 100 and current domestic transaction data.

Interpretation: Prices remain well above long-term averages, but have retreated from recent highs near or above 300, indicating a cooling phase following a prior run-up.

What’s Moving—and What’s Not

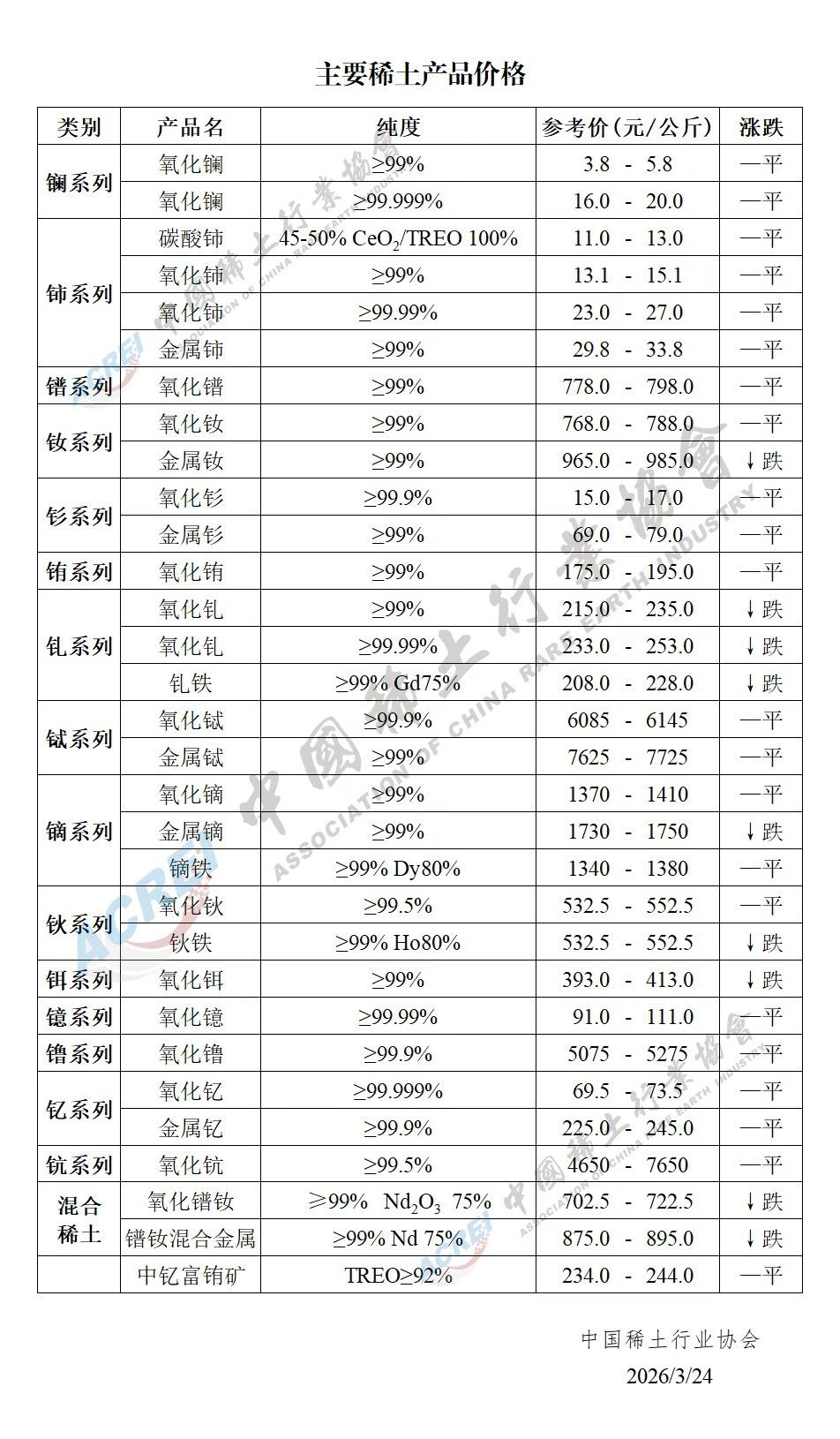

A review of the March 24 pricing table shows a largely stable market with selective declines:

Stable Core Materials

- Cerium oxide, lanthanum oxide, and many light rare earth products: flat (“—平”)

- Several midstream and heavy rare earth oxides: unchanged

This suggests steady baseline industrial demand, particularly for bulk materials.

Selective Weakness in Magnet Inputs

Products showing declines (“↓跌”) include:

- Praseodymium-neodymium (Pr-Nd) related materials, including oxides and alloys

- Gadolinium and terbium-iron intermediates

- Selected rare earth metal products

These materials are closely tied to:

- Permanent magnets (NdFeB)

- EV drivetrains

- Industrial and defense applications

Interpretation: The data points to short-term adjustments—likely inventory, procurement timing, or demand pacing—rather than structural weakness.

Heavy Rare Earths: Largely Stable

- Dysprosium and holmium-related materials: mostly flat. Of course in the West (ex-China) these prices can be far higher as the commodities are harder to obtain.

No immediate supply disruption is visible in this snapshot, though these markets remain structurally tight over longer horizons.

What This Actually Means

This is best understood as a market recalibration, not a breakdown.

1. China Remains the Pricing Center

The index is derived from domestic transaction data—reinforcing China’s role in price formation across the rare earth value chain.

2. Short-Term Volatility Is Normal

Price movements likely reflect:

- Procurement cycles

- Inventory adjustments

- Demand variability in downstream sectors

3. Magnet Materials Bear Watching

Movement in Pr-Nd-related materials highlights ongoing sensitivity in the magnet supply chain, a critical node for global electrification and defense.

Implications for the U.S. and the West

- Western markets remain dependent on externally formed pricing signals

- Short-term price declines do not change structural reliance on Chinese processing capacity

- For EV and defense supply chains:

- Near-term price relief does not equate to long-term supply security

Bottom Line: Cooling Prices, Enduring Leverage

- China’s rare earth prices are easing—but the broader system remains intact.

- This is a moderating market within a concentrated supply structure, not a shift in control.

- The key signal: Volatility may come and go—but structural dominance persists.

What About ‘Ex-China’?

An ex-China rare earth pricing market at scale is not yet realistic because the fundamental conditions required for transparent price discovery simply do not exist outside China. Today, the vast majority of rare earth materials—especially separated oxides, metals, and magnet alloys—are still processed within China, making it the de facto center of liquidity and price formation. Outside China, transactions remain thin, fragmented, and largely bilateral, often governed by long-term contracts, strategic offtake agreements, or government-supported arrangements rather than open-market trading. This leads to opacity in pricing, limited spot market activity, and inconsistent benchmarks.

While there is clear forward momentum—U.S., Australia, and allied nations are investing in separation, metallization, and magnet manufacturing, supported by emerging industrial policy and defense-driven demand—these efforts are still nascent and sub-scale. Yes, a couple of announced price floors help, but remain targeted. Without sufficient volumes, standardized products, and active trading hubs, a true ex-China pricing mechanism cannot yet emerge. In short, progress is real, but until midstream capacity, market liquidity, and independent transaction volume reach critical mass, China will continue to anchor global rare earth pricing.

Disclaimer: This information originates from the China Rare Earth Industry Association, a state-affiliated source. While the data provides useful market visibility, it should be independently verified and interpreted within the context of official Chinese industry reporting.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →