Highlights

- China controls 90% of rare earth processing and dominates critical mineral refining (47–87% across copper, lithium, cobalt, graphite), creating strategic choke points that threaten defense, automotive, semiconductor, and clean energy manufacturers with export licensing delays and production shutdowns.

- High-risk sectors (defense, automotive, semiconductors, clean energy) face acute operational exposure from rare earth magnet shortages, as demonstrated by Ford's production halts and Suzuki's suspensions in 2025, while limited substitutes and long qualification cycles amplify vulnerability.

- Manufacturers must execute five resilience tracks: secure multi-region supply and strategic inventory (Track A), design products for material optionality (Track B), re-architect demand to eliminate rare earth dependency (Track C), control market interfaces and pricing visibility (Track D), and build speed through pre-qualified playbooks and real-time disruption signals (Track E).

So what has changed, and why manufacturers should care now? Rare earth elements (REEs) and “critical minerals” have evolved from commodity inputs into strategic choke points because the tightest constraint is not mining, but midstream processing (separation, refining, alloying) and downstream conversion (especially high-performance permanent magnets). Rare Earth Exchanges™ community members understand rare-earth supply chains are among the least geographically diversified, with China’s position strongest in separation and refining (about 90% of global production at that stage).

This concentration is no longer theoretical: China’s 2025 licensing regime for REEs and magnet products created immediate export friction and visible production impacts. Global automakers warned of factory shutdown risk, and several experienced disruptions tied to rare-earth magnet supply and licensing delays.

The strategic implication for U.S. manufacturing is clearly stated (even by the administration itself): the U.S. may have domestic mining in some areas but lacks sufficient domestic processing capacity to avoid downstream import reliance.

Where China holds the choke points

China’s leverage is amplified because it spans multiple layers of the industrial stack—from refined oxides to metals/alloys to finished magnets—and it extends across non-REE minerals that share infrastructure, chemicals, energy inputs, and permitting bottlenecks. For REEs used in magnets (NdPr, Dy, Tb), China’s dominance is especially acute in processing and manufacturing, with global dependence reinforced by trade exposure (e.g., a very high share of U.S. NdFeB magnet imports sourced from China).

For other critical minerals, China also leads in processing/refining: Rare Earth Exchanges™ has reported that China dominates critical-mineral refining across key materials (copper/lithium/cobalt/graphite/rare earths), with the leading refiner share ranging roughly 47% to 87% depending on the mineral, citing IEA data.

Authoritative commodity statistics reinforce additional chokepoints:

- Gallium: China accounted for ~99% of worldwide primary low‑purity gallium production (a direct semiconductor exposure).

- Silicon materials: China accounted for ~80% of the total global estimated production (broad electronics/solar and metallurgical supply exposure).

- Copper: China produces more than 45% of the world’s refined copper, underpinning electrification and industrial manufacturing.

Export controls and technology restrictions further harden the moat: the U.S. Geological Survey documents China’s restrictions that include rare-earth extraction/separation, rare-earth magnets/compounds, and related mining/processing/smelting technologies.

Meanwhile, the IEA notes export controls have increasingly included gallium, germanium, graphite, and tungsten—minerals tightly coupled to semiconductors, batteries, aerospace, and defense.

Industry survey and risk ranking

REE- and magnet-enabled components are embedded across far more than “clean tech.” The most consistently impacted verticals include: defense & aerospace; automotive (ICE + hybrid + EV); semiconductors & electronics; clean energy (wind, grid hardware, EV supply chain); medical technology; industrial motors & robotics; and telecommunications.

Red (high risk): acute operational exposure + limited substitutes + high likelihood of policy-driven disruption

Defense & Aerospace. The U.S. Department of Defense uses rare earths and other critical materials across weapon systems (radar, guidance systems, precision munitions, lasers, satellites), and our analyses and reporting indicate “military-use” specialized magnet clearance can remain unresolved even when broader trade truces occur. Note that the conflict in the Middle East only intensifies the risk. But as we have suggested to the Trump administration via this platform, there are strategies to consider.

Automotive. 2025 showed the “just-in-time” fragility: Ford Motor Company halted production over rare-earth magnet shortages, Suzuki Motor Corporation suspended production tied to China’s curbs, and Hyundai Motor Company disclosed stockpiling as a mitigation strategy. Honda and others are looking to accelerate the decoupling of the supply chain in China.

Semiconductors & Electronics. Beyond REEs, the sector is exposed to China-dominant inputs (notably gallium; also export-controlled minerals and processing tech), and market moves show immediate sensitivity to REE policy shocks.

Clean Energy Technology. Permanent-magnet traction motors and wind-turbine drivetrains are strongly linked to rare-earth magnets; Europe’s own assessments highlight the dependence of EV motor technology on rare-earth permanent magnets. More companies are approaching Rare Earth Exchanges seeking help with a candid, expedited assessment of actual risk, coupled with a blueprint for supply chain diversification.

Yellow (caution): meaningful exposure, but volumes are smaller and/or buffers are more feasible.

Medical Technology. Risk concentrates in high-spec subsystems and materials used in electronics/lasers and specialty components; disruptions become critical because device certification and supplier qualification cycles are long (even if tonnage is small).

Industrial Motors & Robotics. Exposure is broad (servo motors, precision actuators, factory automation). Risk varies by whether designs can shift away from NdFeB, but performance tradeoffs and requalification timelines push many applications toward “caution.”

Telecommunications. Small amounts can be mission-critical (e.g., yttrium-iron-garnet components used to control high-frequency signals in radar/microwave contexts), so suppliers and specs matter more than tonnage.

Green (low risk): not evident across the listed verticals.

Given recent export frictions and the breadth of embedded magnets/materials, “Green” is generally limited to manufacturers whose products contain trivial REE content, maintain long inventory coverage, and can qualify alternates quickly—conditions that are uncommon in the verticals above.

Risk assessment framework and the signal taxonomy to monitor

A practical scoring model for each vertical (and each product line) in our REEx Insights engine for supply chain combines: (a) material intensity & uniqueness (which elements, which forms: oxide/metal/alloy/magnet), (b) single-point-of-failure nodes (one separator, one metal-maker, one magnetizer, one tier-2), (c) time-to-recover (qualification and regulatory recertification lead times), (d) inventorycoverage (weeks of magnets/components, not just oxides), and(e) allocation probability in a crisis (likelihood of government or prime-contractor priority).

To operationalize rare earth and critical mineral signal detection, monitor five signal classes with measurable triggers:

Geopolitical risk signals: Track export licensing regimes and enforcement intensity (China), plus upstream fragility where Chinese supply chains depend on foreign feedstock (e.g., cobalt/copper nexus in Central Africa).

Supply disruption indicators: Mine shutdowns/permitting delays and, more critically, separation and metal/alloy bottlenecks (where China’s share is highest).

Pricing & market signals: Watch divergence between magnet REEs (NdPr vs Dy/Tb) during licensing frictions; monitor non-linear price reactions typical of concentrated markets and export-control shocks.

Supplier health & credibility signals: Validate “ex-China” capacity claims against commissioning timelines and demonstrated output; recent U.S. efforts remain small relative to China’s scale, implying persistent dependency risk even with new projects. Rare Earth Exchanges™ has expressed concerns about the delta between the U.S. administration chatter and actual realities on the ground.

Technology & substitution signals: Track magnet thrift/reduced Dy/Tb loading, alternative motor topologies, and recycling scale-up; diversification requires both technology progress and policy support as concentration risks rise. How does your company fare on this front?

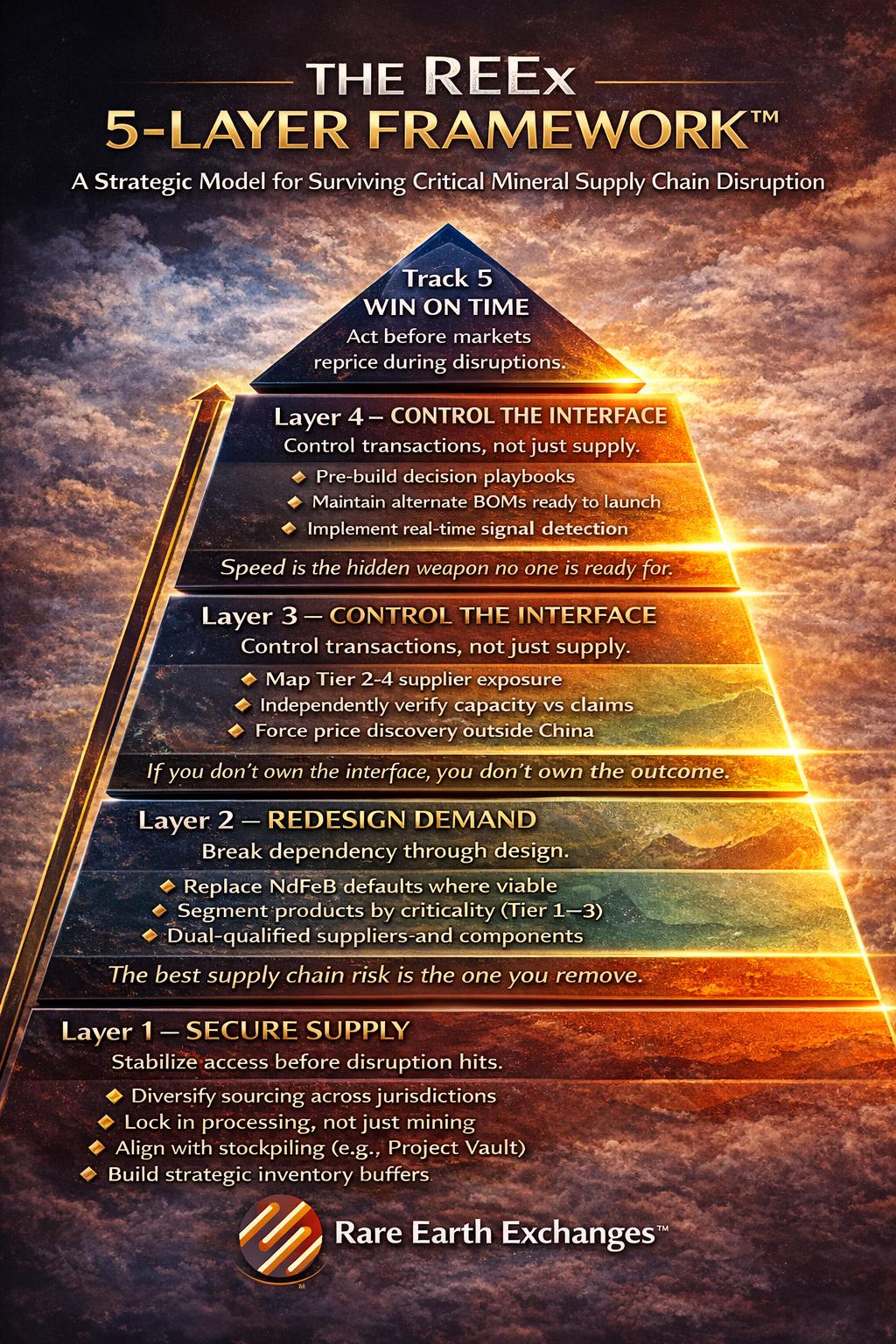

What Manufacturers Should Do Now

First, treat magnets and processed critical minerals as Tier‑N dependencies, not purchasable commodities: decompose every program BOM down to alloy/magnet grade, map the tier chain, and quantify “weeks of coverage” at the component level (motors, sensors, actuators), not just raw material.

Second, execute a dual-track resilience play. Track A: lock in supply via multi-region contracting, qualification of ex-China processors, and strategic inventory policies (including alignment with government stockpiling/market interventions such as “Project Vault”). But remember we are learning to reimagine supply chains in the West---it’s hard, and at the same time, there is more going on than you might assume. Track B: design the next product revision for optionality—multiple magnet grades, motors that can tolerate alternate materials, and certified recycled feedstock pathways.

Every corporation and agency we come across now contemplates triage dynamics. If export controls tighten again, allocation will favor national-security and systemically important manufacturing first; any manufacturer without pre-qualified alternates may be forced into the worst outcome: buying finished subassemblies from the very supply chain they planned to replace—at crisis pricing and with limited negotiating power.

Track C—Demand Re-Architecture—shifts the battleground from supply to design**.** The core insight is that China’s advantage is not just in mining or processing, but in defining the _standards_—magnet types, motor architectures, and performance assumptions—that Western products are built around. As a result, manufacturers have unknowingly engineered dependency into their own systems.

The REEx Track C breaks that paradigm by challenging the default: instead of asking how to secure rare-earth inputs, companies redesign products to reduce or eliminate the need for them altogether—through alternative motor designs, hybrid systems, and material-substitution strategies that prioritize resilience over peak efficiency.

This approach operationalizes “geopolitical survivability” as a design principle. Manufacturers segment products by criticality, reserve rare earths for essential applications, and aggressively substitute elsewhere—potentially reducing exposure by 30–60%. They introduce internal stress pricing and simulate supply shocks to force innovation, while shifting toward modular, adaptive supply networks that allow real-time substitution.

The result when feasible (and many times it’s not) is a fundamentally different posture: not chasing constrained supply, but reshaping demand itself. In a world of tightening export controls, the winners may not be those who secure rare earth access—but those who no longer depend on it. Of course, this latter track represents a long-term, unfolding trajectory, important nonetheless.

Track D & E — The Missing Control Layer

Track D: Control the Market Interface shifts focus from having supply to controlling how supply is accessed, priced, and validated. China’s advantage is not just production—it is opacity, contract leverage, and information asymmetry. Manufacturers must build direct visibility into Tier 2–4 suppliers, independently verify capabilities, secure conversion capacity (not just raw materials), and use platforms like REEx to establish price discovery outside China. The core principle: if you don’t control the interface, you don’t control the outcome.

Track E: Win on Time recognizes that speed—not strategy—determines survival in a disruption. Supply shocksunfold in weeks while qualification cycles take months or years. Manufacturers must pre-build decision-ready playbooks, maintain alternate BOMs ready for activation, and deploy real-time signal detection (pricing divergence, export controls, supplier stress). The winners will be those who act before the market reprices—everyone else will be forced to buy from the new producers at crisis premiums.

Conclusion — The Strategic Reality

Even with Tracks A, B, and C—let alone D and E, the uncomfortable truth remains: the West cannot replicate China’s system fast enough. China controls scale, cost curves, processing depth, and industrial coordination. The goal, therefore, is not full independence—but selective dependence paired with strategic escape velocity.

In a tightening export environment, allocation will follow power: defense first, then systemically important OEMs, leaving the rest exposed. At that point, markets clear through China—at a premium. The only durable strategy is layered: secure what you must, redesign what you can, and eliminate dependency where possible—while controlling information and moving faster than disruption.

Resilience isn’t just securing supply—it’s controlling how, when, and whether you need it at all.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →