Highlights

- Rare earth supply chains fail not at mines but in solvent extraction plants where chemical separations depend on specific reagents like P204 and P507 extractants that cannot be easily substituted.

- China's 2025 export controls explicitly target critical separation chemicals including extractants and reagents, creating administrative leverage over global rare earth processing capacity.

- Western capacity building faces chemical ecosystem challenges: concentration in bulk chemicals like oxalic acid and ammonium chloride creates vulnerabilities beyond just mining operations.

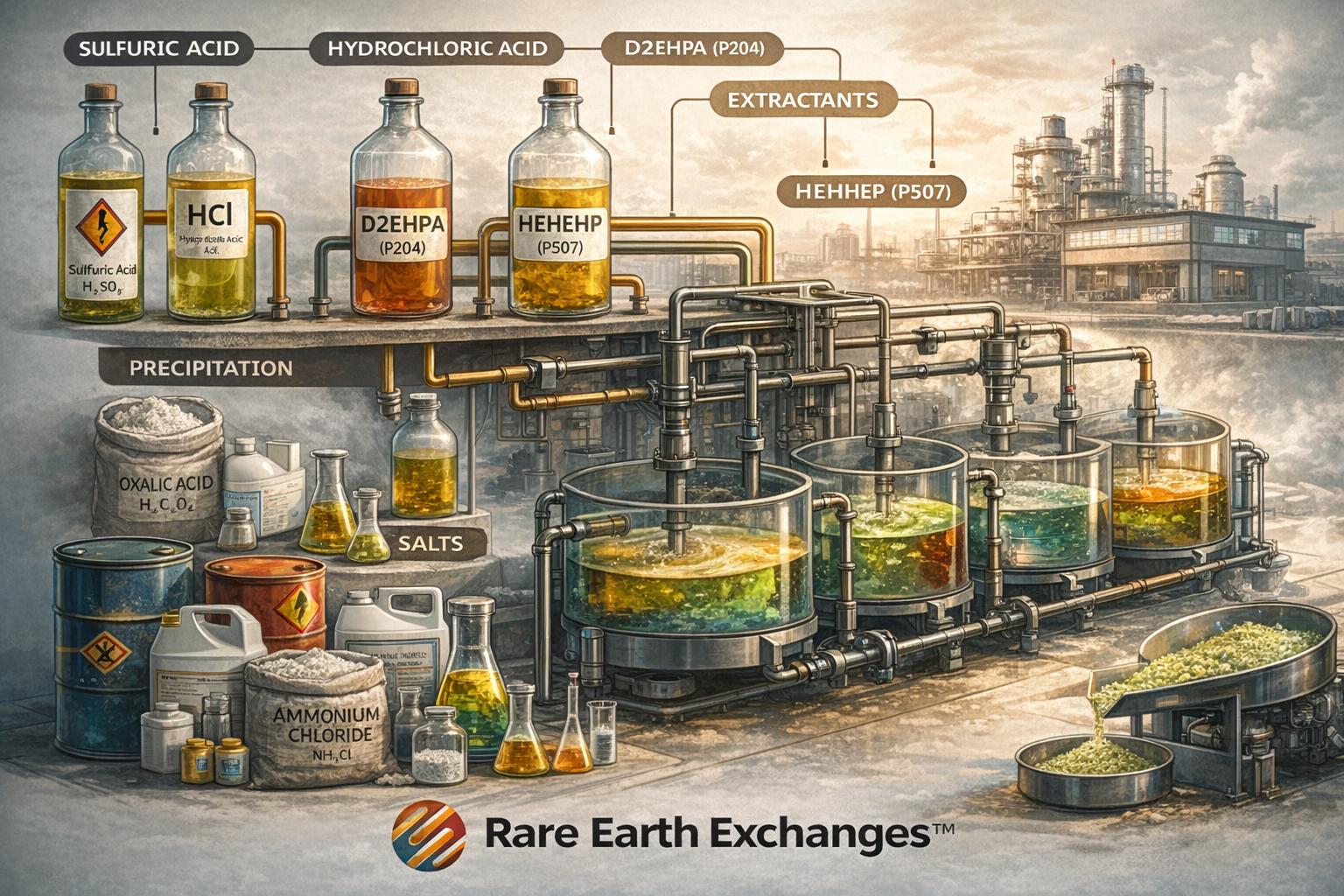

Rare earth supply chains don’t usually fail at the mine. They fail downstream—inside solvent extraction (SX) plants, where 17 chemically similar elements are separated through hundreds of stages. Building a mine is hard. Separating rare earths into usable materials is harder—and far more fragile. SX is not just infrastructure. It is a reagent-dependent system: acids, extractants, diluents, salts, and precipitation agents. Change one input, and the entire flowsheet can shift—stage count, purity, waste streams, and economics.

Industry reality remains unchanged: extractants like D2EHPA (P204) and HEHEHP (P507) are core to commercial separation. These are not interchangeable inputs. They are embedded process logic.

The Shift: Export Controls Move Into Chemistry

Since 2023, policy has caught up with chemistry.

- 2023: China restricts rare earth processing and magnet technologies

- April 2025: Licensing controls applied to medium/heavy rare earth materials

- October 2025: Export controls expand to include extractants and flotation reagents, explicitly naming P204 and P507

- November 2025: Temporary suspension (not repeal) signals policy optionality

This matters.

When a government names specific molecules in export controls, chemistry is no longer theoretical leverage—it is operational leverage. And the pattern is now clear: tighten → disrupt → selectively reopen.

The Chemicals That Quietly Control Throughput

Not all choke points are exotic.

Some are industrial-scale, low-cost inputs that become critical through concentration.

Oxalic acid

- Used in precipitation stages across refining flows.

- China exported ~298 million kg in 2023 (WITS data).

- Other suppliers exist—but at far smaller scale.

Ammonium chloride

- A “basic” chemical used in impurity control.

- China exported ~966 million kg in 2023.

- Export concentration—not chemistry complexity—creates vulnerability.

Extractants (P204/P507)

- The real constraint is qualification, not availability.

- Substitution risks process instability across hundreds of SX stages.

- The pattern is consistent: Global availability does not equal industrial reliability

Case Studies: When Policy Hits Production

2025 offered real-world validation.

- Export licensing delays halted shipments

- Rare Earth Exchanges™ noted downstream impacts: automakers faced magnet shortages, some reduced production

- China introduced magnet tracking systems—compliance as friction

- “Streamlined licenses” later restored flows—on Beijing’s timeline

Even the European Union created a dedicated channel with China to prioritize approvals—an extraordinary admission that licensing had become a supply chain variable.

This is not geology. This is administrative control layered onto chemical dependence.

Can the West Break Free—or Just Rebrand Dependence?

- Progress is real (and early stages)—but also constrained.

- The data shows refining remains highly concentrated, with >90% still controlled by a handful of countries—primarily China.

- Western projects are emerging (U.S., Malaysia, Estonia, Canada and Australia), but midstream capacity remains nascent.

What actually changes the equation:

- Domestic/allied production of extractants and reagents

- Strategic stockpiles sized for ramp risk—not steady state

- Faster permitting for chemical plants and waste systems

- Qualification of alternative chemistries before disruption

Emerging R&D (e.g., Oak Ridge National Laboratory) may reduce stage count—but remains early-stage.

Separating Signal from Narrative

What’s now strongly supported:

- Chemical concentration is measurable (oxalic acid, ammonium chloride)

- SX complexity is real (hundreds of stages)

- Export controls now explicitly include reagents

Where caution is needed:

- Bulk chemical restrictions remain situational, not guaranteed

- Market adaptation and substitution are possible—but slow

The real risk is not immediate shutdown. It is delayed scaling.

REEx Final Take: Chemistry Is the Control Layer

Mining gets headlines. Chemistry decides outcomes.

The West is not just rebuilding supply chains—it is rebuilding chemical ecosystems under regulatory and time constraints.

You don’t lose a supply chain when the mine shuts down alone. You also lose it when the chemistry stops working. And that failure rarely announces itself in advance.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →