Highlights

- The rare earth bottleneck is magnet qualification, not ore supply.

- China controls 85-90% of sintered permanent magnet production through an integrated industrial learning system that spans ore to finished magnets.

- China's advantage stems from state-backed pilot lines like Baotou's facilities that reduce iteration costs, enabling rapid prototyping and OEM qualification cycles that Western projects cannot match.

- America needs a magnet proving ground—an integrated facility for separation, alloy-making, prototyping, and motor validation—because stockpiles alone won't solve the metallization-to-qualification gap.

Could the real rare-earth bottleneck not be ore but rather qualification? Rare earth magnets are not commodity blocks; they are application-specific systems. The key variables are coercivity, maximum energy product, operating temperature, corrosion behavior, geometry, coating stack, and the precise use of heavy rare earths such as dysprosium and terbium. With magnet design comes a trade-off among coercivity, energy product, operating temperature, weight, and cost. EV traction motors typically require higher-grade magnets, often with 6% or more dysprosium, due to the thermal environment. In other words, the user’s “custom cake” analogy is technically right.

That is why qualification takes so long. China remains dominant — at about 85-90% of sintered permanent magnet production in 2025, 91% of refined magnet rare-earth output, and an even tighter grip on downstream magnet making. Rare Earth Exchanges™ has suggested that ex-China capacity would cover only a small fraction of projected magnet demand outside China by 2035. Magnet manufacturing and metallization are acute bottlenecks in the value chain.

China built an ecosystem for learning speed

China’s advantage is not only cheap output or scale. It is an industrial learning system. The 2024 Rare Earth Management Regulations place mining, smelting and separation, metal refining, comprehensive utilization, circulation, imports, and exports under a unified national framework, while the 2025 draft rules on total-control quotas and traceability tighten coordination even further. That gives Chinese producers a policy spine that links ore, oxide, metal, alloy, and magnet decisions instead of treating them as isolated businesses.

At the local level, Baotou shows how the system turns policy into speed. City support measures give deep-processing companies priority access to praseodymium-neodymium raw materials from Northern Rare Earth, two months of supplier credit with municipal interest support, subsidies for lanthanum and cerium purchases, and direct grants for innovation platforms. This is state backing aimed not only at stockpiling material, but at keeping pilot runs and first commercial campaigns alive long enough to learn.

Why is China so hard to catch? Outside projects face higher costs and weaker demand certainty, while projects in China benefit from industrial ecosystems, low-cost energy and inputs, skilled labor, vertical integration, shared infrastructure, strong balance sheets, and large domestic offtake bases. That is the real answer to “how China does it.” China reduced the cost of iteration.

The Chinese Pilot Lines REEx Now Studies

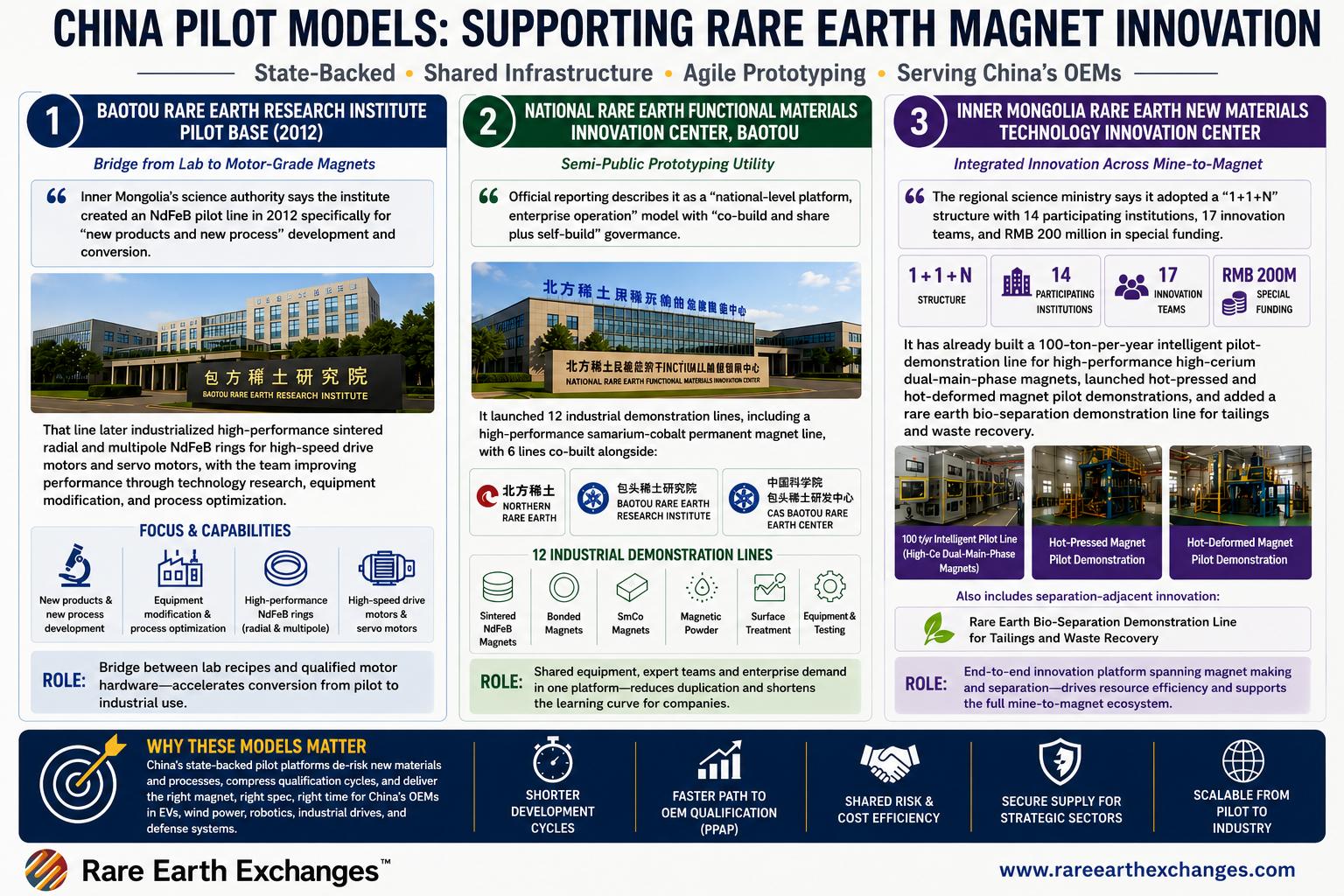

The clearest example is the Baotou Rare Earth Research Institute pilot base. Inner Mongolia’s science authority says the institute created an NdFeB pilot line in 2012 specifically for “new products and new process” development and conversion. That line later industrialized high-performance sintered radial and multipole NdFeB rings for high-speed drive motors and servo motors, with the team improving performance through technology research, equipment modification, and process optimization. This is not a conventional factory; it is a bridge between lab recipes and qualified motor hardware.

A second model is the National Rare Earth Functional Materials Innovation Center in Baotou. Official reporting describes it as a “national-level platform, enterprise operation” model with “co-build and share plus self-build” governance. It launched 12 industrial demonstration lines, including a high-performance samarium-cobalt permanent magnet line, with six lines co-built alongside Northern Rare Earth, the Baotou Rare Earth Research Institute, and the CAS Baotou Rare Earth Center.

Simply, China created a semi-public prototyping utility that can pull in expert teams, shared equipment, and corporate demand without forcing every company to finance the whole learning curve alone. A third model is the newer Inner Mongolia Rare Earth New Materials Technology Innovation Center. The regional science ministry says it adopted a “1+1+N” structure with 14 participating institutions, 17 innovation teams, and RMB 200 million in special funding. It has already built a 100-ton-per-year intelligent pilot-demonstration line for high-performance, high-cerium dual-phase magnets, launched hot-pressed and hot-deformed magnet pilot demonstrations, and added a rare-earth biosorption demonstration line for tailings and waste recovery. That is striking because it spans not only magnet making but also learning about separation-adjacent processes.

Even the academic literature helps explain why these pilot lines create value. Recent reviews show that Ce-containing and multi-main-phase NdFeB routes are central to balancing China’s rare earth resource mix, while grain-boundary diffusion remains one of the main tools for cutting Dy and Tb usage without giving up temperature performance. Reviews of hot-deformed NdFeB make the same point for radially oriented rings and shape-intensive applications. China’s pilot lines are valuable because they are organized around these exact learning problems: mixed-rare-earth chemistry, heavy-rare-earth thrift, and near-net-shape magnet architectures.

One more case matters. China Iron & Steel Research Group (opens in a new tab) spent years developing cerium magnets (opens in a new tab) and then brought them to market through partnerships with Ningbo Funeng (opens in a new tab) and Shandong Shangda. By 2017, Ningbo Funeng had licensed production of 6,000 tonnes of the new Ce magnet, and by 2023, domestic Ce-magnet output had surpassed 60,000 tonnes annually (opens in a new tab). That is the Chinese pattern in miniature: state research takes the technical risk, partner plants absorb the scaling risk, and the market learns by doing.

The OEM feedback loop is embedded in production

China’s magnet champions then turn those platform capabilities into customer-facing speed. JL MAG (opens in a new tab) says it operates make-to-order production, controls product R&D through testing and component production, and helps customers optimize performance while lowering cost; more than 90% of its 2024 output used grain-boundary diffusion technology, and its raw-material base is anchored by long-term relationships with Northern Rare Earth and China Rare Earth Group. Ningbo Yunsheng (opens in a new tab) describes itself as providing highly customized NdFeB application solutions to major EV brands and traction-motor makers. ZHmag (opens in a new tab) says its products are mostly custom, non-standard parts made to customers’ overall system requirements through design, R&D, production, and after-sales integration.

This factory-to-OEM loop is reinforced by organized demand matching. At the 2023 Baotou Rare Earth Industry Forum, 20 supply-demand cooperation projects were signed alongside industrial and research agreements. Meanwhile, local government reports cite rare-earth projects commissioned in 86 days and motor parks moving from contract to steel structure in roughly 60 days. Not every Chinese magnet producer is an SOE. But even private or mixed-ownership firms operate within a state-shaped system that lowers the cost of accessing raw materials, conducting pilot learning, customer sampling, and mobilizing industrial land and utilities.

America needs a magnet proving ground

The United States is not starting from zero. The Pentagon said in March 2024 that it had awarded more than $439 million since 2020 to build a domestic mine-to-magnet chain, with investments spanning separation, recycling, magnet making, and e-VAC’s metals-and-alloys-to-magnets capability. MP Materials and its Pentagon deal is real, but its larger Texas “10X” campus is not expected to begin commissioning until 2028. And Frankly, meeting qualification at scale could be a year or two away.

Europe offers a similar lesson: Neo shipped EV traction-motor-grade samples from Estonia in April 2025, targeted PPAP in the first half of 2026, and only commissioned a small-scale heavy-rare-earth separation line in April 2026. Qualification is sequential, slow, and capital-hungry even when progress is genuine.

That is why Project Vault, however useful as a strategic buffer, is not enough. A roughly $12 billion stockpile structure designed to hold critical minerals for emergency access. That may cushion shocks (assuming it does not lead to hoarding and speculation), but by design, it does not solve the metallization-to-alloy-to-prototype-to-PPAP gap.

The evidence points to a second institutional need: an American magnet proving ground. That facility should integrate small- to mid-scale separation, metallization, alloy-making, sintered- and bonded-prototyping, machining, coating, magnetic testing, and motor validation under one roof, with government-backed learning budgets and open access for qualified OEM programs. Stockpiles buy time. Pilot bakeries win qualification. China understood that years ago. Rare Earth Exchanges will ensure America builds one.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →