Highlights

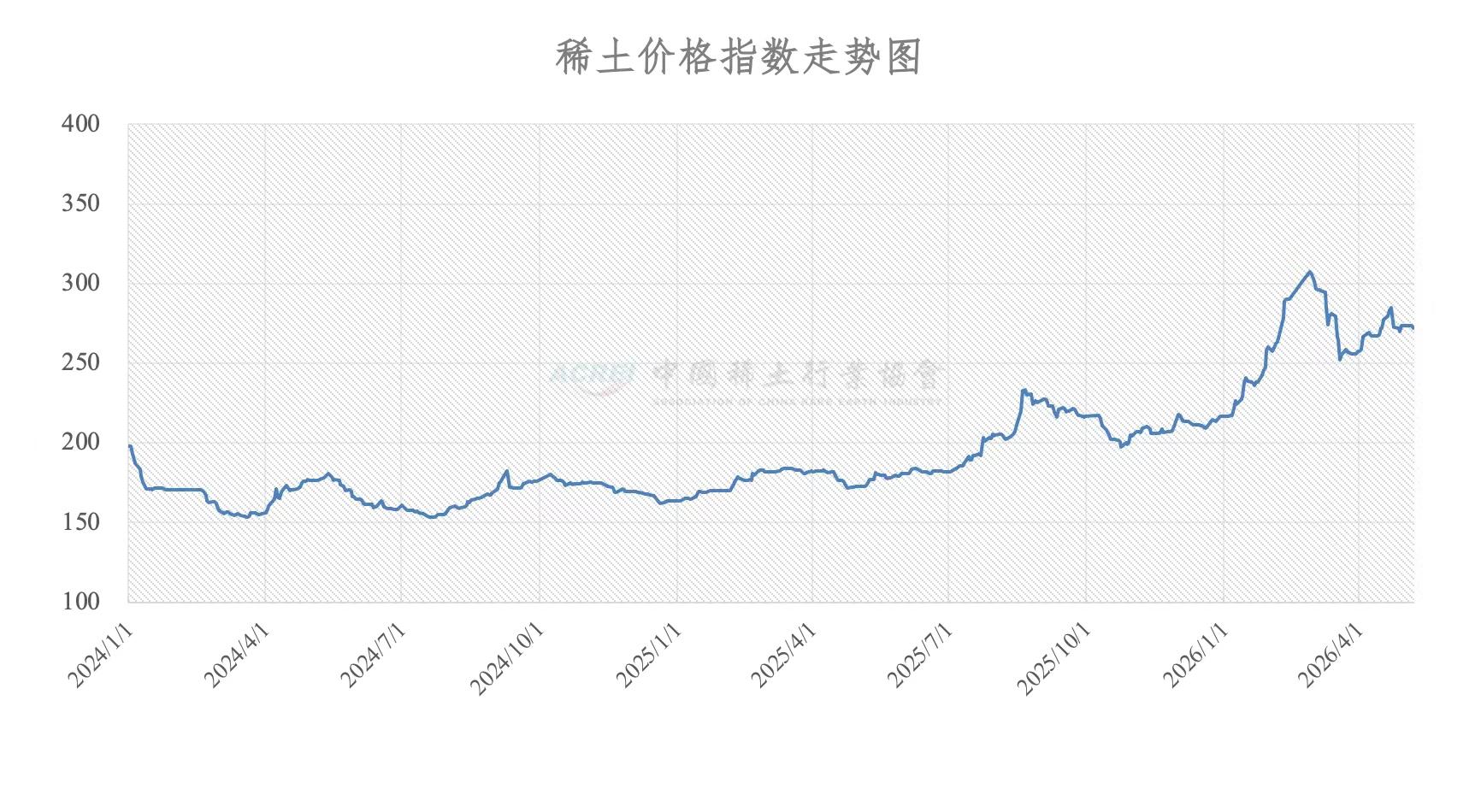

- China's rare earth price index reached 271.8 on May 7, remaining historically elevated despite recent moderation from 2026 peaks above 300, reflecting continued structural tightness in a market where China controls 90% of global processing capacity.

- Critical heavy rare earths like dysprosium and terbium showed softening prices but remain extraordinarily expensive and strategically essential for EV drivetrains, defense systems, wind turbines, and AI-era industrial automation.

- China's rare earth pricing operates under extensive state influence rather than as a transparent free market, with policy objectives, export controls, and production quotas shaping prices—highlighting persistent geopolitical vulnerability for Western manufacturers dependent on Chinese supply chains.

China’s official rare earth price index rose to 271.8 on May 7, according to new figures released by the China Rare Earth Industry Association. While the number itself may appear technical, the broader trend is strategically important: China’s domestic rare earth pricing environment remains historically elevated compared to pre-2025 levels, despite growing volatility across individual elements.

The index—calculated using transaction data from domestic Chinese rare earth enterprises and benchmarked against 2010 pricing levels set at 100—suggests that rare earth markets remain structurally tight even as certain heavy rare earth categories weaken.

A Market Still Running Hot

The accompanying pricing chart shows China’s rare earth index climbing sharply over the past 18 months, peaking above 300 earlier in 2026 before moderating modestly to current levels near 272. That matters because China still controls roughly 90% of global rare-earth processing and separation capacity, along with a dominant share of downstream permanent-magnet manufacturing. Movements in China’s domestic pricing environment continue to ripple through EV supply chains, defense procurement, robotics manufacturing, wind turbines, semiconductors, and advanced electronics worldwide. For Western manufacturers, the key takeaway is not simply price direction—it is persistent structural vulnerability and supply-chain concentration.

Heavy Rare Earths Show Early Signs of Softening

Several critical heavy rare earth products moved lower in China’s latest pricing data, signaling potential short-term weakness in parts of the strategic magnet materials market. Dysprosium oxide was quoted around 1.34–1.38 million yuan per metric ton (approximately $185,000–$191,000 USD), while terbium oxide remained extraordinarily elevated near 6.08–6.14 million yuan per ton (roughly $840,000–$848,000 USD) despite modest daily declines. Gadolinium-related products also softened. Note pricing ex-China is substantially higher.

These materials remain among the most strategically important inputs in the global industrial economy. Dysprosium and terbium are essential for high-performance permanent magnets capable of operating under extreme heat and stress conditions—making them indispensable for EV drivetrains, missile guidance systems, aerospace platforms, robotics, drones, wind turbines, and emerging AI-era industrial automation infrastructure.

At the same time, many lighter rare earth categories remained comparatively stable. This suggests China’s domestic rare earth market may be entering a more selective, segmented pricing phase rather than a broad-based downturn across the entire complex.

The Pricing Caveat: This Is Not a True Free Market

Perhaps the most important nuance is structural rather than numerical. China’s rare-earth pricing system does not operate like a transparent global commodity market, such as oil, copper, or gold. The industry operates under extensive state influence, export licensing controls, production quotas, environmental enforcement campaigns, and strategic industrial oversight. Rare-earth pricing within China remains heavily shaped by policy objectives, state-linked enterprises, and opaque bilateral commercial relationships.

There is also no deep, liquid global futures market for rare earth oxides or magnets comparable to those for major industrial commodities. As a result, price discovery remains fragmented and often non-transparent.

Outside China, the market is still immature and developing. Ex-China pricing often arises through confidential bilateral contracts among miners, refiners, magnet manufacturers, automakers, and governments. Terms often vary significantly by purity, processing stage, delivery security, financing arrangements, and geopolitical considerations. Some Western projects also involve policy-linked pricing support, strategic floor-price structures, or government-backed offtake agreements.

In effect, the global rare earth market increasingly resembles a strategic industrial ecosystem rather than a conventional free-market commodity sector.

The Bigger Story: China Still Anchors the Global Benchmark

China’s rare earth price index is therefore best understood not as a universal global benchmark, but as the dominant pricing reference inside a highly concentrated and strategically managed industrial system. For the United States and Europe—still deeply dependent on Chinese refining, separation, alloying, and magnet production—the index serves as a reminder that rare earth supply chains remain geopolitically sensitive, opaque, and structurally asymmetric.

Disclaimer: This pricing information originates from the China Rare Earth Industry Association, a Chinese state-linked industry body. Reported prices, methodologies, and market conditions should be independently verified through commercial transactions, technical disclosures, and external market intelligence providers.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →