Highlights

- Modern missile manufacturing depends on sprawling global supply chains spanning semiconductors, specialty chemicals, industrial gases, magnets, and precision equipment—not just rare earth mining—with MBDA alone relying on approximately 4,000 suppliers.

- China controls critical industrial bottlenecks beyond raw materials, including 60% of global PCB fabrication and key rocket propellant binders, creating geopolitical leverage points that could disrupt Western defense production.

- Rebuilding Western missile supply chain independence requires decades of investment across midstream chemistry, metallization, electronics fabrication, and specialized engineering—far beyond simple mining initiatives.

A new analysis by Lucie Béraud-Sudreau (opens in a new tab) at the International Institute for Strategic Studies, (opens in a new tab) an England and American-based think tank, warns that modern missile production depends on vast, deeply interconnected global supply chains—not simply rare earth mining or final weapons assembly. Drawing on examples from European missile giant MBDA (opens in a new tab) and broader defense-industrial data, the report argues that contemporary missile manufacturing requires a sprawling network of semiconductors, specialty chemicals, industrial gases, magnets, explosives, batteries, printed circuit boards (PCBs), advanced materials, and precision manufacturing equipment sourced from across the world. The analysis highlights a growing strategic vulnerability for the West: China and other geopolitical chokepoints increasingly dominate not only critical raw materials, but also the chemicals, components, and industrial processes required to transform those materials into deployable weapons systems. For lay readers, the takeaway is straightforward but profound—modern defense manufacturing resembles a tightly interconnected industrial nervous system, where disruptions in one sector can rapidly cascade into missile shortages elsewhere.

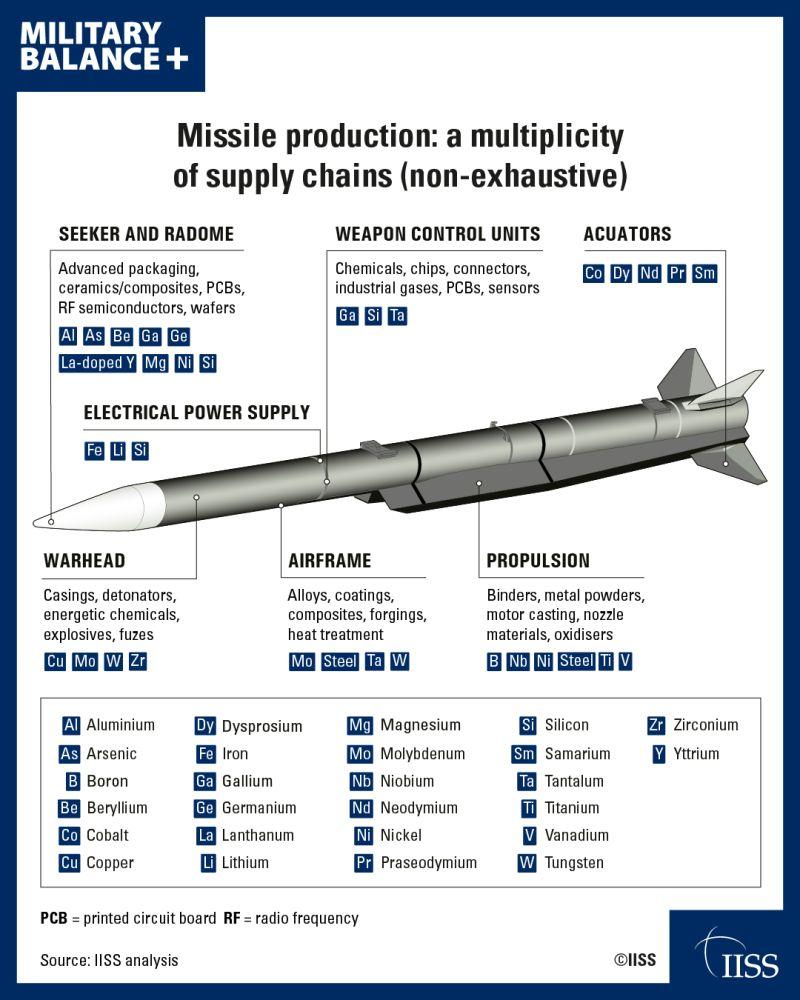

The Missile Is Really Thousands of Supply Chains

The IISS analysis breaks missile production into multiple industrial layers, each dependent on separate upstream and midstream ecosystems. Seekers and radomes require advanced ceramics, semiconductors, gallium, germanium, yttrium, and silicon. Actuators depend heavily on rare earth elements such as dysprosium, neodymium, praseodymium, and samarium used in high-performance magnets. Propulsion systems require boron, niobium, titanium, vanadium, steel, oxidizers, and specialized binders.

Even seemingly mundane components such as printed circuit boards rely on globally distributed supply chains involving chemicals, laminates, copper processing, semiconductor packaging, and precision fabrication.

MBDA reportedly operates through a supplier network of approximately 4,000 companies, underscoring how no single nation fully controls the entire missile-production stack.

China’s Leverage Extends Far Beyond Rare Earths

One of the report’s most important conclusions is that critical raw materials are only “the tip of the iceberg.” Far greater vulnerabilities may lie in hidden industrial bottlenecks such as PCB fabrication, industrial gases, chemicals, precision manufacturing equipment, and specialized process knowledge.

The study notes that roughly 90% of global PCB manufacturing occurs in Asia, with China alone accounting for nearly 60% of worldwide production. Military-grade hydroxyl-terminated polybutadiene (HTPB)—a critical rocket propellant binder—also suffers from an extremely narrow supplier base, creating additional risks for Western missile manufacturing.

This matters because geopolitical conflict, export controls, shipping disruptions, industrial accidents, or regulatory shocks can ripple across the defense ecosystem. The report specifically cites Middle East instability affecting sulfur and sulphuric acid shipments, which in turn impact copper extraction, semiconductor fabrication, battery manufacturing, and military explosives production.

Strategic Implications for the West

For Rare Earth Exchanges™ readers, the analysis reinforces a core reality: the rare earth challenge is not fundamentally a mining problem. It is an industrial systems problem. Western governments frequently announce ambitious “mine-to-magnet” initiatives, yet the report demonstrates that modern defense manufacturing depends equally on midstream chemistry, metallization, alloying, electronics fabrication, coatings, industrial gases, advanced machinery, and highly specialized engineering talent.

Rebuilding these ecosystems could require decades of investment, workforce development, permitting reform, and coordination across defense, trade, energy, and industrial ministries.

Limitations and Remaining Questions

The report is primarily a strategic industrial assessment rather than a quantitative economic model. It does not fully estimate the costs, timelines, or political tradeoffs required to rebuild Western supply chains at scale. Nor does it deeply examine whether full reshoring is economically realistic given the efficiencies of globally integrated manufacturing.

Some critics may also argue that diversified global supply chains can create resilience rather than vulnerability alone. However, the report suggests that excessive concentration—particularly in China—has transformed many industrial dependencies into potential leverage points in geopolitics. Still, the central warning is difficult to ignore: missiles may be assembled in America or Europe, but many of the industrial arteries feeding those production lines remain globally exposed.

Citation: Lucie Béraud-Sudreau, International Institute for Strategic Studies, “Defense supply chains beyond CRMs: dependencies and bottlenecks,” Military Balance+ Blog, May 6, 2026.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →