Highlights

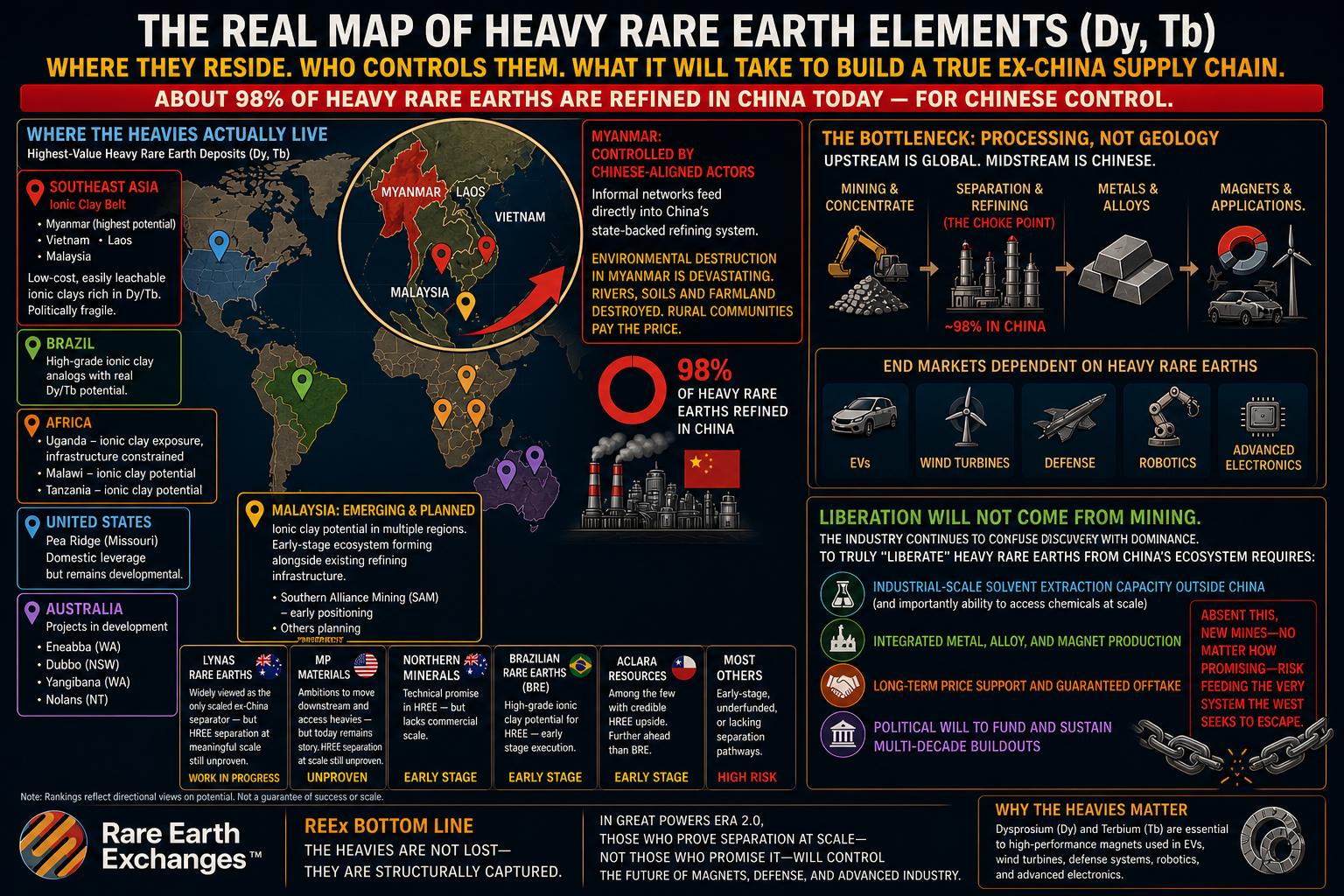

- 98% of heavy rare earths (dysprosium, terbium) remain refined in China despite global deposits in Myanmar, Brazil, Uganda, and the U.S.—geology isn't the constraint, processing infrastructure is.

- High-value ionic clay deposits exist across Southeast Asia, Brazil, and Africa, but without industrial-scale separation capacity, new mines risk feeding China's existing system.

- True supply chain liberation requires proven separation capability at scale, integrated metal/alloy/magnet production, and sustained political commitment—not just promising new discoveries.

This analysis exposes where heavy rare earths (Dy, Tb) actually reside, who controls them, and what it will take to build a true ex-China supply chain. Built for investors navigating the most misunderstood bottleneck in critical minerals.

Heavy rare earths are not scarce—they are concentrated, controlled, and poorly understood. The world’s most critical magnet inputs—dysprosium and terbium—remain anchored in southern China and the adjoining belts of Myanmar, where informal networks feed directly into China’s state-backed refining system. This is the uncomfortable truth: the upstream story is global, but the midstream remains Chinese. About 98% of heavy rare earths today continue to be refined in China, for Chinese supply chain controls.

Where the Heavies Actually Live

The highest-value heavy rare-earth deposits are located in ionic clay systems across Southeast Asia—Myanmar, Vietnam, Laos, and Malaysia. These are low-cost, easily leachable, and rich in Dy/Tb. But they are also politically fragile and, in Myanmar’s case, effectively controlled by actors aligned with Chinese processing demand. The environment and rural communities are also paying a devastating ecological price. For all the talk in China of green and sustainability, when it comes to lands across the border, they become less concerned and look the other way.

Outside Asia, credible alternatives are emerging:

- Brazil — high-grade ionic clay analogs with real Dy/Tb potential

- Africa: Uganda — ionic clay exposure but infrastructure constrained; plus Malawi, Tanzania

- United States — assets like Pea Ridge offer domestic leverage but remain developmental

- Australia—projects in development (Eneabba, Dubbo, Yangibana, Nolans)

- Malaysia—Southern Alliance Mining, new projects in the works

But here’s the catch: geology is not the constraint—processing is.

The Scorecard Investors Miss

A recent DFARS-focused ranking alongside the REEx Insights rankings places Pea Ridge as a possible asset due to its integrated U.S.-based potential and HREE capability. That’s directionally important—but not yet reality.

Across the global landscape:

- Lynas Rare Earths is widely viewed as the only scaled ex-China separator—but its ability to consistently deliver heavy rare earth separation at meaningful scale remains a work in progress, not a fully proven industrial outcome.

- MP Materials signals ambitions to move downstream and access heavies—but today remains fundamentally a light rare earth (LREE) story, with HREE separation at scale still unproven. Investors in the REEx community (which is growing by the day) will monitor MP very carefully for evidence of capability and, importantly, execution on this topic.

- Northern Minerals shows technical promise—but lacks commercial scale.

- Brazilian Rare Earths (BRE) and Aclara Resources are among the few with credible HREE upside—but remain early in execution. Aclara is further ahead than BRE, although we believe both show potential.

In short: even the market leaders _signal capability_—but have yet to fully demonstrate repeatable, large-scale heavy rare earth separation outside China.

Liberation Will Not Come From Mining

The industry continues to confuse discovery with dominance.

To truly “liberate” heavy rare earths from China’s ecosystem requires:

- Industrial-scale solvent extraction capacity outside China (and importantly, the ability to access chemicals at scale)

- Integrated metal, alloy, and magnet production

- Long-term price support and guaranteed offtake

- Political will to fund and sustain multi-decade buildouts

Absent this, new mines—no matter how promising—risk feeding the very system the West seeks to escape.

REEx Bottom Line

The heavies are not lost—they are structurally captured.

And in Great Powers Era 2.0, those who prove separation at scale—not those who promise it—will control the future of magnets, defense, and advanced industry.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →