Highlights

- The U.S. may need $2 trillion to rebuild manufacturing capacity in rare earths, semiconductors, batteries, and advanced materials lost to decades of offshoring.

- China now controls roughly 90% of global rare earth refining and permanent magnet production, while the U.S. still lacks critical midstream processing capabilities.

- Rare earth permanent magnets—essential for AI servers, EVs, drones, and defense—are conspicuously absent from most rebuilding roadmaps despite their strategic importance.

- Western dependence on Chinese rare earth refining and magnet manufacturing is projected to persist well into the next decade despite recent investment momentum.

- Capital can build factories, but rebuilding the engineers, metallurgists, supplier networks, and industrial know-how lost over 40 years will take far longer than any election cycle.

McKinsey estimates the United States may need roughly $2 trillion to rebuild manufacturing capacity across strategically important industries. Yet the more important question is not how much rebuilding will cost. It is how America lost these capabilities in the first place. For rare earths, critical minerals, batteries, semiconductors, and advanced materials, the challenge is no longer constructing factories. It is rebuilding industrial ecosystems that were allowed to migrate overseas over several decades.

Source: At One Ventures

The $2 Trillion Bill Arrives: America Pays for Three Decades of Offshoring

America's industrial revival has received a price tag: roughly $2 trillion.

Investors should look past the headline. The real story is not the cost of rebuilding. It is the cost of dismantling. Many of the institutions now warning about supply-chain vulnerabilities spent decades championing globalization, outsourcing, and hyper-efficient global production networks.

In 2003, McKinsey published research arguing that offshoring generated net economic benefits for the United States and created value for every dollar moved abroad. At the time, the logic appeared sound. Labor costs fell. Margins expanded. Inflation remained contained. Wall Street rewarded the strategy.

Meanwhile, China quietly converted manufacturing into national strategy.

The Industrial Muscle America Exported

Rare earths provide perhaps the clearest example of what was lost. The United States did not fall behind because China possessed unique geology. America once held leadership positions in rare earth mining, refining, metal-making, alloy production, magnet manufacturing, and advanced materials.

What migrated overseas was industrial capability. Today, China controls approximately 90% of global rare earth refining and permanent magnet production. The United States has made meaningful progress in mining and early-stage processing, but the most critical segments of the value chain—separation, refining, metallurgy, alloy production, and magnet manufacturing—remain overwhelmingly concentrated in China.

The missing link is not the mine.

It is the midstream.

Forty Years of Compounding Versus Four-Year Election Cycles

McKinsey correctly notes that capital may be the easy part. The difficult task is rebuilding engineers, metallurgists, operators, machine shops, supplier networks, industrial parks, transmission infrastructure, and technical know-how. China compounded these advantages over four decades while much of the West optimized for quarterly earnings and increasingly short political cycles.

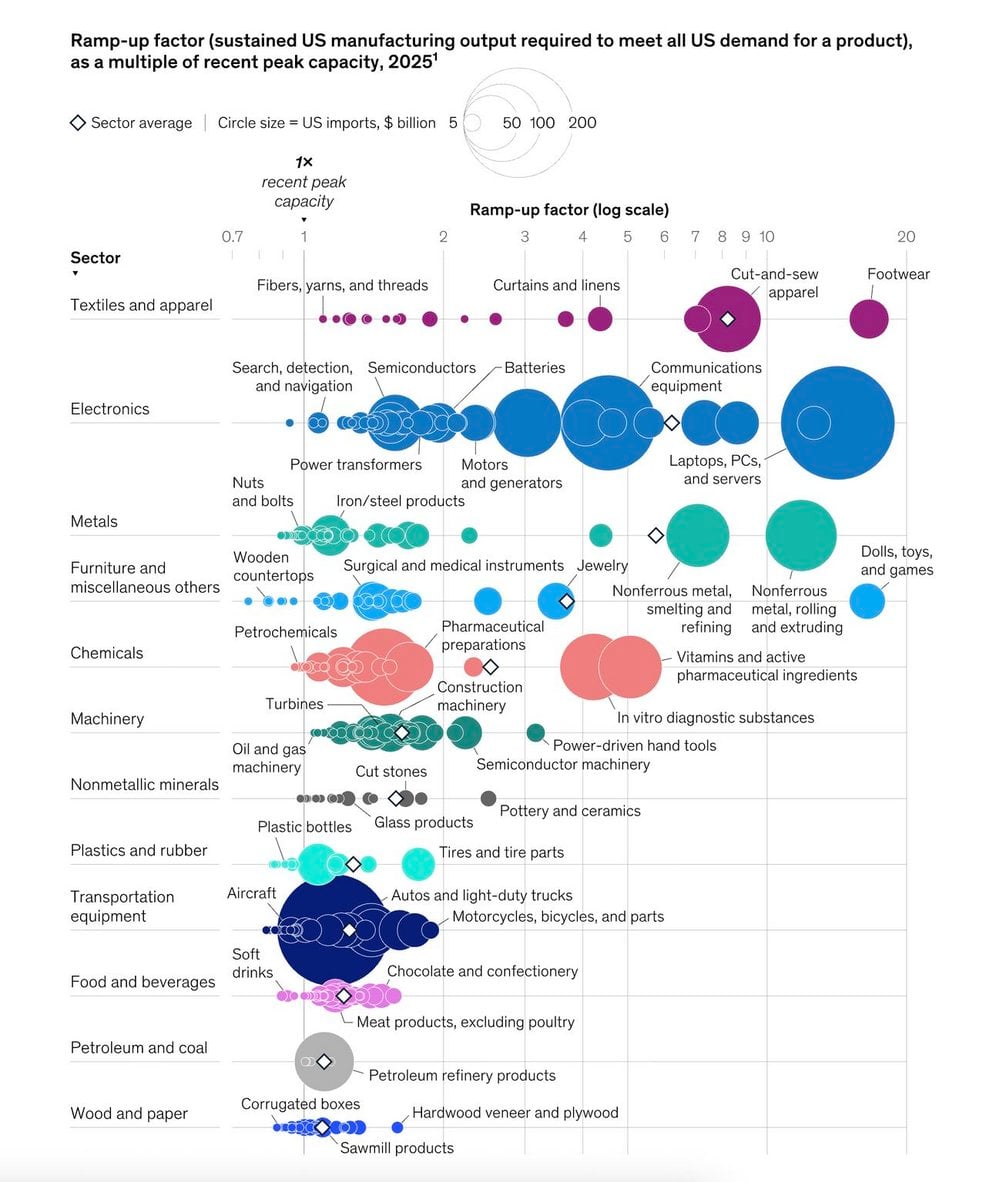

One notable omission from the chart above is rare earth permanent magnets.

Yet magnets sit inside AI servers, robotics, drones, electric motors, communications equipment, advanced manufacturing systems, and modern defense platforms. Without magnets, these industries do not scale. Without refining, magnets do not scale. Without metallurgical expertise, refining does not scale.

The supply chain is only as strong as its weakest link.

The REEx Bottom Line

The irony is difficult to miss. The same globalization movement that helped justify offshoring now estimates it may cost $2 trillion to rebuild what was lost. And even that figure may understate the challenge. Based on current project pipelines, permitting timelines, workforce constraints, capital requirements, and processing capacity, Western dependence on Chinese rare earth refining, magnet manufacturing, and critical mineral processing is likely to persist well into the next decade. Progress is real, but the gap remains enormous.

Money can build factories. Industrial capability takes generations.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →