Highlights

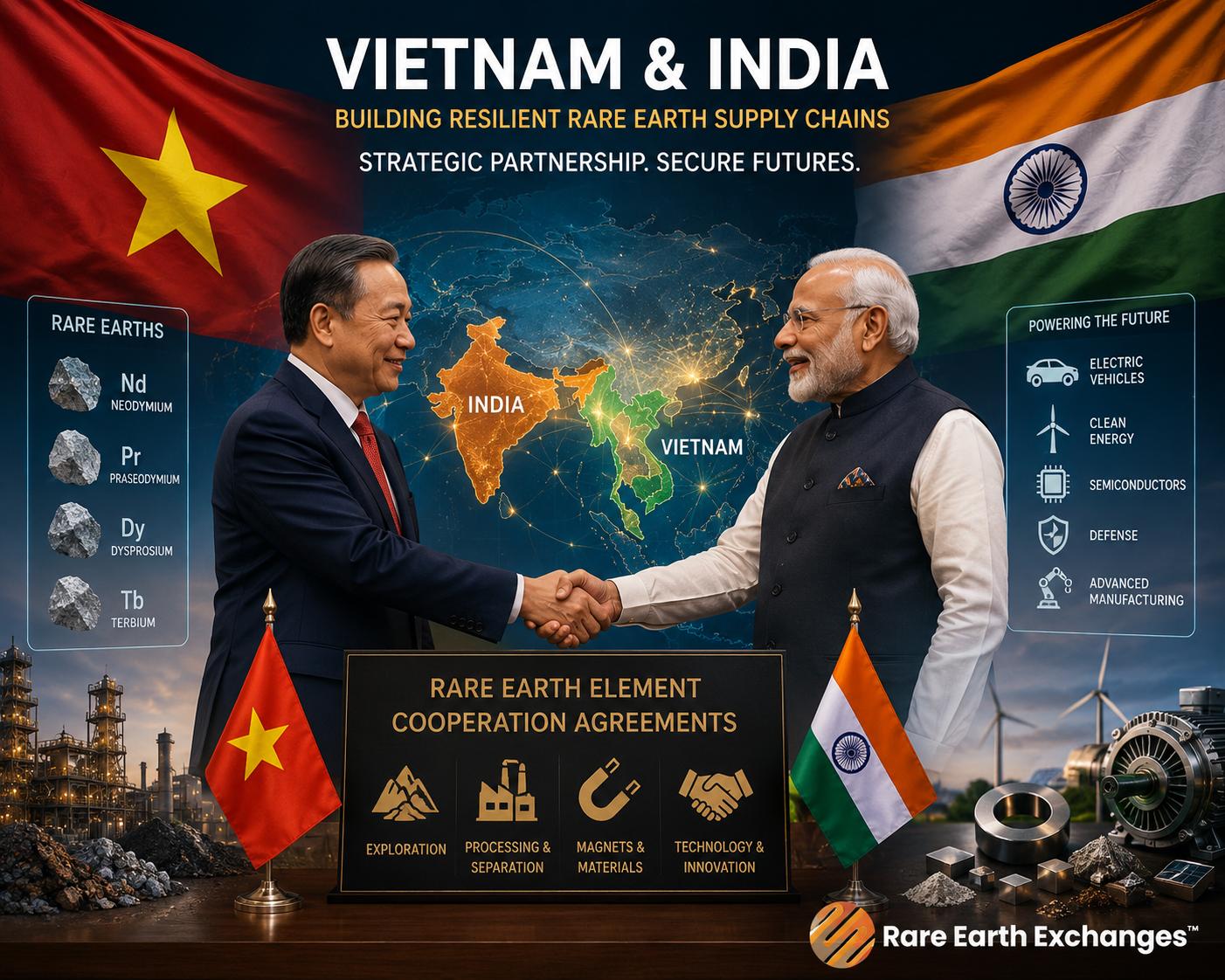

- Vietnam and India signed 13 cooperation agreements, including a rare earth partnership, reflecting how supply chains have evolved from commercial networks into instruments of statecraft in the Great Powers Era 2.0.

- While China controls 90% of global rare-earth processing capacity, the real strategic value lies in midstream capabilities such as separation, metallurgy, and magnet production rather than raw mineral deposits.

- Strategic middle powers are positioning themselves as indispensable within reconfigured Indo-Pacific supply chains, understanding that future geopolitical winners will control industrial corridors and refining ecosystems, not just minerals.

The next global power map may not be written solely in oil pipelines, naval fleets, or semiconductor fabs. Increasingly, it is being etched through rare earth separation plants, logistics corridors, payment systems, refining alliances, and industrial ecosystems invisible to most consumers but essential to modern civilization.

Source: Vietnam Investment Review

This week, Vietnam and India signed 13 cooperation agreements spanning digital technology, finance, pharmaceuticals, tourism, education—and notably—rare earth cooperation. Buried deep inside the bureaucratic architecture of the deal sits a strategically important agreement between Vietnam’s Institute of Rare Elements and IREL (India) Limited.

That detail matters far more than it may initially appear.

The Quiet Geometry of Great Powers Era 2.0

India wants supply-chain resilience, industrial depth, and geopolitical leverage. Vietnam wants diversification, foreign capital, technological advancement, and strategic flexibility. Both increasingly understand the same emerging truth: supply chains are no longer passive commercial networks. They are instruments of statecraft.

The article correctly highlights expanding cooperation across digital infrastructure, payment systems, technology, and logistics. But the deeper story is industrial positioning within a fragmenting global order.

Vietnam is practicing what REEx describes as “strategic middle-power optimization”—leveraging geography, manufacturing capability, diplomatic agility, and trade access to become indispensable inside reconfigured Indo-Pacific supply chains. India, meanwhile, continues attempting to evolve from resource consumer into industrial counterweight.

Mines Are Easy. Midstream Is the Empire.

The coverage, however, risks oversimplifying what “rare earth cooperation” actually means in practice.

An MoU is not a refinery. A deposit is not metallization. And geology alone does not meaningfully weaken China’s structural dominance.

China still controls roughly 90% of global rare-earth separation and processing capacity and dominates permanent magnet manufacturing. The true chokepoints remain solvent extraction chemistry, heavy rare-earth separation, alloying, magnet production, and downstream qualification.

Still, the trend itself matters enormously.

Tier-one powers and ambitious middle powers alike are now racing to secure industrial relevance before today’s supply-chain fragmentation hardens into tomorrow’s geopolitical architecture.

In the Great Powers Era 2.0, the ultimate winners may not simply own the minerals.

They may own the corridors, relationships, refining ecosystems, and industrial chains surrounding them.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →