Highlights

- The Nacala Corridor, spanning Mozambique, Malawi, and Zambia, is positioned as a next-generation critical minerals model backed by the African Development Bank and Japan, aiming to capture value locally through integrated logistics and governance—yet currently lacks the commercial-scale refining and processing capacity needed to truly compete.

- Infrastructure alone does not confer power: without solvent extraction separation, rare earth refining systems, or downstream manufacturing, the corridor risks becoming merely a more efficient export route for raw materials rather than a value-capturing industrial ecosystem.

- The project signals a structural shift as African nations reject the extract-and-export model and demand local value capture, but until midstream chemical processing is built at industrial scale, these alternative supply chains remain incomplete and unable to challenge China's vertically integrated dominance.

A railway in southeastern Africa is attempting something the West still struggles to execute: build a real mineral supply chain—not just extract ore and ship it abroad.

Source: Africa Center for Strategic Studies, “Reciprocal and Resilient Mineral Supply Chains: Lessons from the Nacala Corridor,” April 13, 2026.

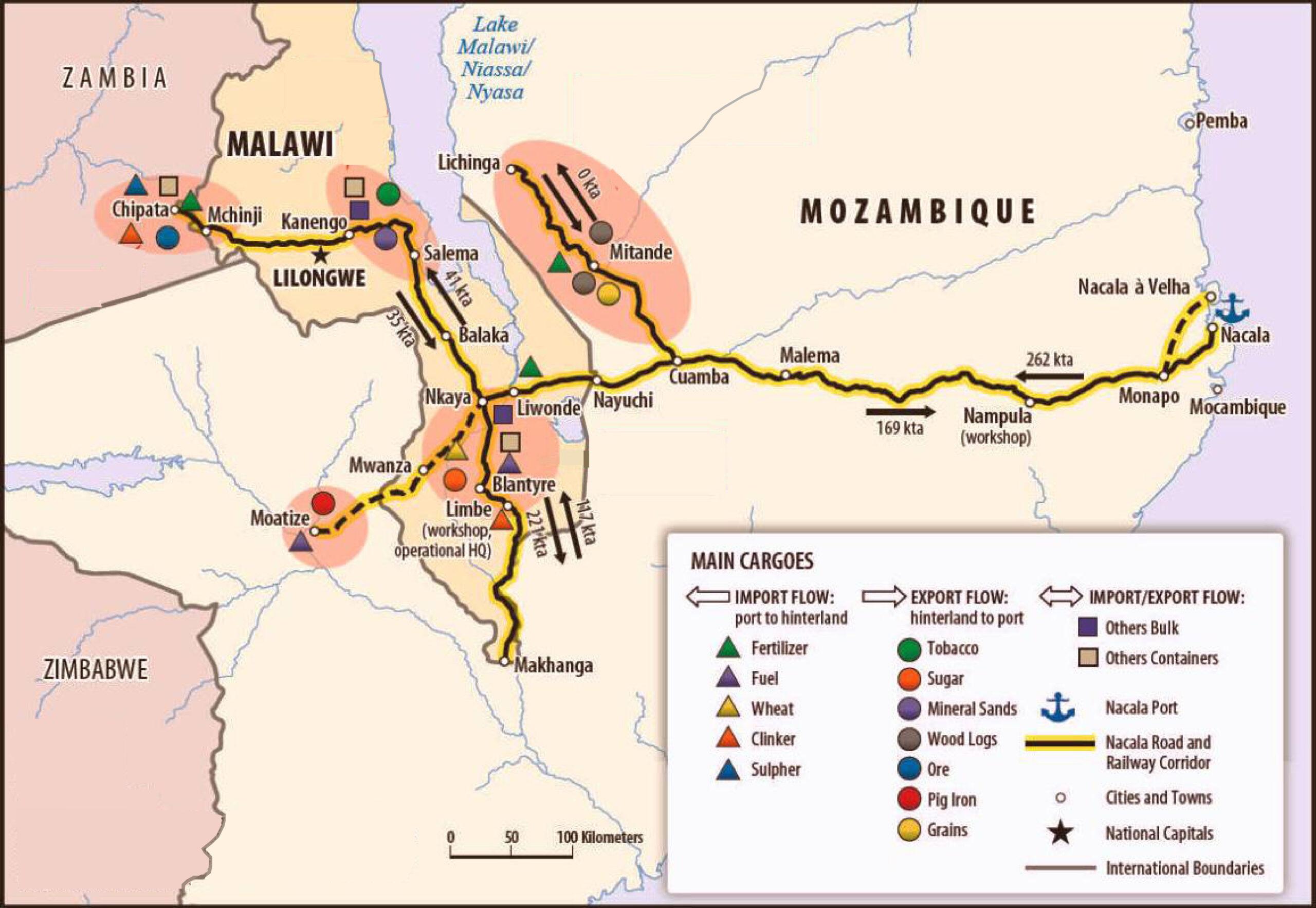

The Nacala Corridor, linking Mozambique, Malawi, and Zambia to a deepwater Indian Ocean port, is being positioned as a next-generation critical minerals model—one designed to capture value locally, improve transparency, and evolve into a full “mine-to-market” ecosystem. Backed by institutions such as the African Development Bank and the Japan International Cooperation Agency as reported (opens in a new tab) by the Africa Center for Strategic Studies (opens in a new tab), the corridor integrates transport infrastructure, regulatory checkpoints, and early-stage industrial ambition into a single regional system.

Key Nodes and Strategic Opportunities: The Nacala Corridor

| Country | Ports & Terminals | Rail Infrastructure | Road Networks | Special Zones/Trade Nodes | Key Production Areas | Strategic Value Capture Opportunities |

|---|---|---|---|---|---|---|

| Mozambique | Port of Nacala; Nacala-a-Velha Terminal | Moatize–Nacala rail; Nampula–Nacala rail | Muita–Mandimba–Lichinga Road; Cuamba–Mandimba–Lichinga Road; feeder roads linking mines and farms | Nacala Special Economic Zone | Coal (Moatize); Graphite (Balama); Mineral sands (Moma) | Develop midstream graphite processing and battery materials manufacturing near port infrastructure |

| Malawi | Access via Port of Nacala (through Mozambique) | Malawi–Mozambique rail links via Nsanje, Entre-Lagos, and Chiponde–Mandimba (connecting Lilongwe & Blantyre to corridor) | Feeder roads connecting agricultural zones to rail terminals; upgraded border facilities at Entre-Lagos | Border trade hubs (Entre-Lagos crossing) | Tobacco, tea, sugar, cotton | Expand agro-mineral logistics integration; enable future rare earth and mineral export scaling |

| Zambia | Access via Port of Nacala (through Malawi & Mozambique) | Chipata–Mchinji rail link; planned Chipata–Serenje extension connecting Copperbelt to corridor | Chipata–Lusaka Road axis; part of SADC Route 20 corridor (Sinda–Petauke–Nyimba–Rufunsa corridor) | Regional transport integration via SADC network | Copper; cobalt | Expand DRC–Zambia EV battery corridor; attract precursor processing and battery materials assembly near mining zones |

Source: Africa Center for Strategic Studies, “Reciprocal and Resilient Mineral Supply Chains: Lessons from the Nacala Corridor,” April 13, 2026.

At its core, the thesis is simple—and strategically correct: move beyond extraction, build processing capacity, and retain value in-country.

Where the Analysis Holds Firm

The article correctly anchors itself in the defining reality of modern mineral geopolitics: mining alone does not confer power—processing does.

China’s dominance is not primarily geological. It is industrial. Control over separation, refining, and downstream magnet production—not ore deposits—defines leverage. The Nacala concept, with its emphasis on integrated logistics, traceability, and potential midstream development, aligns with a hard truth Rare Earth Exchanges has consistently emphasized: without midstream capacity, there is no functioning supply chain.

It is also accurate that Africa is shifting posture. Export restrictions, local beneficiation policies, and political pressure to capture more value are accelerating across the continent. The economic incentive is stark—lithium concentrate at roughly $3,000 per ton versus refined chemical products exceeding $25,000–$30,000 per ton.

That spread is not a margin—it is sovereignty.

The Elegant Vision—Missing Its Industrial Core

Where the narrative overreaches is in its implied causality: that infrastructure plus governance will naturally lead to industrialization.

It will not.

The corridor today lacks the elements that actually determine value capture in rare earths and adjacent critical minerals:

- No commercial-scale solvent extraction (SX) separation capacity

- No established rare earth refining system

- No downstream metal, alloy, or magnet manufacturing base

This is not a minor gap. It is the gap.

Logistics corridors move volume. Industrial systems create value. Without chemical processing at scale, the Nacala Corridor risks becoming a more efficient conduit for raw or semi-processed exports—improving flow, but not fundamentally changing positioning in the global value chain.

The Subtle Tilt: Partnership as Strategy—or Narrative?

The piece leans—quietly but clearly—toward elevating the Japanese development model as a superior alternative: more transparent, more collaborative, more sustainable.

There is merit here. Governance, traceability, and co-development frameworks matter.

But investors should interrogate a more fundamental question:

Can this model compete—on cost, throughput, and speed—with China’s deeply entrenched, vertically integrated system?

Because in critical minerals, comparative advantage is not philosophical—it is operational.

Why This Signals a Structural Shift

Even with its limitations, the Nacala Corridor reflects a deeper inflection point in global supply chains:

The extract-and-export model is being actively rejected. African nations are demanding value capture. Japan is pursuing diversification without direct confrontation. Western policymakers are searching for resilience in a system they no longer control. But the conclusion remains unchanged—and unavoidable:

Until midstream processing is built—chemically, economically, and at an industrial scale—these systems remain incomplete.

And in rare earths, incomplete systems do not compete.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →