Highlights

- China has deliberately built a 40-year strategic monopoly on rare earth elements by subsidizing extraction, investing in research, and controlling the entire supply chain from mining to magnet production.

- The United States currently lacks comprehensive infrastructure to challenge China's rare earth dominance, with projections suggesting full supply-chain resilience may not be achieved until 2040.

- China's rare earth strategy extends beyond materials, positioning the country to potentially control the financial architecture of green and digital economies through strategic commodities control.

China’s October 9 announcement tightening export controls on additional rare earth elements and magnet-related technologies (opens in a new tab) was more than bureaucratic maneuvering — it was a reminder, timed with surgical precision before trade talks with the United States, of just how deeply Beijing controls the material arteries of the modern world.

From smartphones to fighter jets, electric vehicles to wind turbines, every industrial future the West claims to lead runs through China’s rare earth complex. As Rare Earth Exchanges (REEx) has chronicled since its late 2024 launch, this is not coincidence — it is the result of a forty-year national strategy that has fused industrial planning, state capital, and environmental tolerance into global dominance. When will the rest of us get it?

A Monopoly Built on Design, Not Luck

In the 1980s and 1990s, as Western nations shuttered high-pollution mines and outsourced processing to Asia, China did the opposite. It subsidized extraction, poured state funding into refining and metallurgical research, and absorbed short-term losses in the name of long-term control. China started to notice Japan’s intrigue in some waste rock and dirt—and the payload associated with accessing the material. And the rest is history.

By the time the West woke up to its dependence, China controlled over 90% of the world’s rare earth refining and metal processing capacity. REEx analysis shows that Beijing’s dominance was not limited to raw materials — it extended across the value chain:

| Segment of Supply Chain | Summary |

|---|---|

| Upstream (Mining) | China produces roughly 60% of global rare earth ore, with integrated projects like Bayan Obo and Mianning producing at scale and feeding domestic refiners. |

| Midstream (Separation & Refining) | The choke point. Beijing’s state-owned firms — China Northern Rare Earth, Minmetals, and Southern Rare Earth Group — control the purification chemistry Western producers long abandoned. |

| Downstream (Metals & Magnets) | China commands over 90% of neodymium-iron-boron (NdFeB) magnet production, the component backbone for EVs, drones, and defense electronics. |

This dominance translates not just into export leverage, but into pricing power, data access, and the ability to dictate global technological standards — advantages that ripple across every vertical dependent on high-performance materials.

The Western Catch-Up Mirage

REEx has repeatedly warned that tariffs and slogans cannot substitute for strategy. The U.S. under President Donald Trump has done more than any administration in decades — the Department of Defense’s 15% ownership stake in MP Materials, the expansion of Lynas USA’s Texas separation facility, and dozens of critical minerals grants are meaningful steps. But they remain tactical reactions to a structural problem.

At present, the U.S. lacks:

| What’s Missing | Summary |

|---|---|

| Feedstock depth | Beyond MP Materials and nascent Energy Fuels projects, there’s limited ore throughput. |

| Refining infrastructure | Chemical separation capacity in the U.S. remains negligible compared to China’s industrial clusters in Inner Mongolia, Jiangxi, and Sichuan. |

| Metallization know-how | The specialized metallurgical expertise and skilled labor needed to convert oxides into alloys and magnets are scarce. |

| Coordinated policy | Fragmented programs across DoD, DOE, and Commerce often overlap without achieving full integration. |

REEx’s projections suggest that, at current momentum, the U.S. will not achieve full supply-chain resilience — mining through magnets — before 2040. With an aggressive, coordinated industrial policy aligned across allies, that horizon could move to 2035, but only barely. Perhaps earlier—say by 2032 should an Operation Warp Speed type of model be embraced by the U.S. government. One that would be global in focus.

What Tariffs Can’t Fix

Tariffs may create pressure, but they cannot manufacture chemistry. They do not build solvent-extraction circuits, metallization furnaces, or the technical workforce needed to run them. Nor can they substitute for patient capital — the kind Beijing deployed for decades to build its rare earth base.

As REEx has reported often since its founding last year_,_ the West’s current approach risks reinforcing its own dependency. High import costs on Chinese materials raise downstream prices, but without domestic capacity to replace them, the result is inflation, not independence. And to rebuild this specialized supply chain takes more than just markets and money.

Industrial Policy or Industrial Fantasy

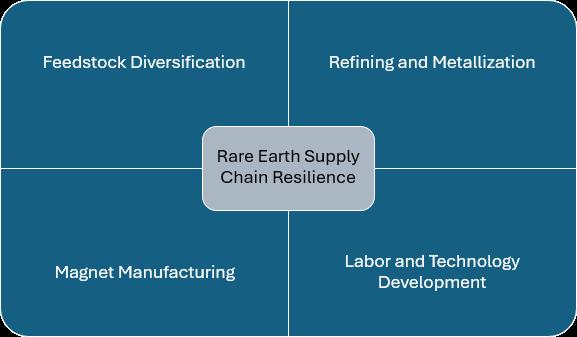

If the West hopes to rebalance the rare earth equation, it must move beyond reactionary crisis management. What’s needed is an industrial policy that fuses national strategy along with international collaboration, along with private capital — one that views the rare earth sector as critical infrastructure, not a boutique niche for ESG funds.

Such a policy must integrate:

- Feedstock Diversification: Secure raw material supply through strategic partnerships with Australia, Canada, and Africa.

- Refining and Metallization: Invest in regional “processing corridors” modeled on China’s Baotou cluster, co-locating separation, alloying, and recycling.

- Magnet Manufacturing: Establish guaranteed offtakes and defense-backed procurement to stabilize pricing for Western producers.

- Labor and Technology Development: Rebuild chemical and metallurgical expertise through university and vocational programs tied to industrial hubs.

REEx’s June 2025 report, “Mine-to-Magnet Integration: The Missing Middle,” concluded that without a globally coordinated approach led by the U.S., the West’s rare earth ambitions will remain fragmented — and vulnerable to every policy twitch from Beijing.

The Broader Play: From Magnets to Money

China’s rare earth monopoly is not merely about materials — it’s about leverage. By controlling the inputs to the green and digital economies, Beijing positions itself to dominate the next financial architecture as well. As outlined in REEx’s translated review of China’s Rare Earth Development Plan 2035, the Communist Party envisions a “strategic commodities corridor” underpinning both industrial production and digital currency governance. Rare earths, in their calculus, are the connective tissue linking energy transition to economic ascendancy.

The Hard Truth

We need to emphasize that the Chinese are not villains in this story — they simply played the long game. It was the West that outsourced, deregulated (and regulated), and rationalized itself into dependency. Now, as export controls tighten once again, the world faces the bill for forty years of complacency. Where is the accountability for that?

Catching up will require something far rarer than neodymium or dysprosium: vision, discipline, coordination, and the courage to think beyond electoral cycles and quarterly dollars and cents. The next decade will determine whether the West rebuilds its industrial backbone — or becomes a permanent customer in China’s metallic marketplace.

© 2025 Rare Earth Exchanges™ – Accelerating Transparency, Accuracy, and Insight Across the Rare Earth & Critical Minerals

0 Comments