Highlights

- The global uranium market's strategic power lies in midstream processing—conversion and enrichment—not upstream mining, with Russia, France, China, and the Urenco consortium dominating this critical control layer.

- While Kazakhstan produces 40% of global uranium, the decisive battleground is the middle of the supply chain where uranium becomes usable nuclear fuel, creating structural dependencies.

- U.S. uranium self-sufficiency faces a 2030-2032 timeline due to limited domestic conversion and enrichment capacity, despite recent federal backing for expansion through Urenco and Centrus Energy.

The global uranium market is often misunderstood as a mining story. It is not. In the Rare Earth Exchanges™ “Great Powers Era 2.0” framework, control sits not in ore, but in the processing and control of exports. Upstream supply is concentrated but relatively diversified. Kazakhstan remains dominant, producing roughly 40% of global uranium, followed by Canada and Namibia. Australia and Uzbekistan round out the top tier. At the corporate level, Kazatomprom (opens in a new tab) (Kazakhstan), Cameco (opens in a new tab) (Canada), and Orano (opens in a new tab) (France) anchor global production. This layer is concentrated—but not strategically decisive.

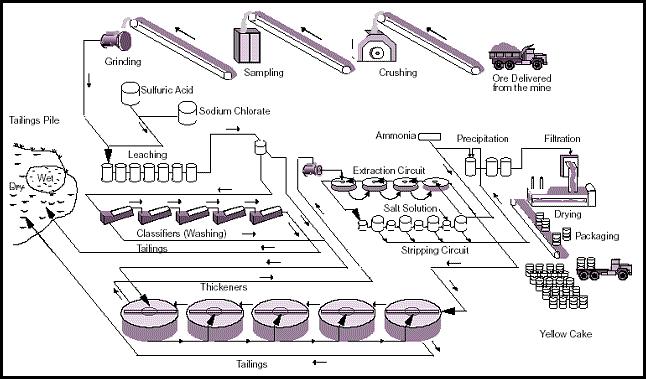

Uranium Mill Process

Source: Energy Information Administration, Office of Coal, Nuclear, Electric, and Alternative Fuels

Power consolidates in the midstream. Conversion and enrichment—where uranium becomes usable nuclear fuel—are dominated by a small group: Russia, France, China, the Urenco consortium (opens in a new tab) (notably the Netherlands, the UK, and Germany), and to a lesser extent the United States. Russia retains structural leverage through enrichment exports, even as Western buyers diversify. Europe’s own agencies warn replacement capacity will take years—not months.

Downstream fuel fabrication is more distributed but still anchored by a handful of players: Westinghouse Electric Company (opens in a new tab), Framatome (opens in a new tab)(France), and Russia’s TVEL (opens in a new tab) (Russia). Here, qualification and reactor compatibility—not volume—create lock-in.

Applying the REEx ranking lens:

- Upstream (scale-driven): Kazakhstan, Canada, Namibia lead

- Midstream (control layer): Russia, France, and China dominate

- Downstream (technology lock-in): U.S., France, Russia lead

The asymmetry is clear: mining is competitive; processing is strategic.

For the United States, the gap is structural. Domestic mining exists but is marginal. Conversion has only recently restarted. Enrichment capacity is limited, though expanding via Urenco (opens in a new tab) (UK) and Centrus Energy (opens in a new tab) (USA), with federal backing from the Department of Energy.

The timeline is not political—it is industrial.

- Allied resilience: plausible by 2028–2030

- Meaningful U.S. self-sufficiency: 2030–2032

Full independence sooner is unlikely, given permitting, construction, and qualification cycles.

The conclusion aligns with the Great Powers Era thesis: alignment is not control, and access is not sovereignty. In uranium—as in rare earths—the decisive battleground is not extraction. It is the middle of the chain.

0 Comments

No replies yet

Loading new replies...

Moderator

Join the full discussion at the Rare Earth Exchanges Forum →